Insurance live transfers sound simple. A person is on the phone, and your licensed agent answers.

The problem is that “insurance” is not one market. Health, Medicare, final expense, life, auto, home, and business insurance each work differently. Each one has different prices, rules, risks, and agent needs.

Buy the wrong call type, and your team can waste money fast. Agents may sit idle, take calls from the wrong state, miss consent issues, or get calls that were not checked well enough.

This guide explains insurance live transfers in plain terms. For the larger model, use the foundational live transfer methodology before comparing insurance campaigns. Then look at price, lead quality, compliance, and provider fit before you buy.

Direct Answer: Insurance live transfers work when you choose the right insurance type, confirm consent, match call volume to licensed agents, and track cost per new policy instead of cost per call.

What Insurance Live Transfers Are

Insurance live transfers are real-time calls from people who have shown interest in an insurance product. The call is sent to a licensed agent while the person is still on the phone.

A vendor, call center, publisher, or lead partner creates the inquiry first. The source may be search, paid ads, direct mail, inbound calls, or follow-up calls. A rep checks the key details, then sends the call to the buying agency.

The agency does not get a lead file. It gets a live phone call.

That is the main difference from internet insurance leads, shared leads, or aged leads. Regular leads still require the agency to call, reach out, check, and close with the person. Live transfers remove part of the contact problem, but they do not remove the work.

That is why the live transfers vs regular lead comparison matters before you compare prices. If you need the basic category first, start with the general live transfer leads category.

Live transfers are only better when the call is checked, allowed, and sent to the right agent. If not, they become costly distractions.

What Buyers Often Confuse With Live Transfers

Insurance agencies often mix several lead types together:

- Internet insurance leads: Form leads that need follow-up calls.

- Aged insurance leads: Older leads are sold at a lower price.

- Shared leads: Leads sold to more than one agent or agency.

- Warm transfer insurance leads: Calls screened by a live rep before transfer.

- Inbound phone calls: Calls from the agency’s own marketing.

- Live transfer calls: Calls sent in real time by a vendor or call center.

This matters because each lead type has a different reach rate, close rate, and cost. Internet leads may look cheaper. But if your team reaches only a few of them, the cost per new policy can rise fast.

That is also why handling aged leads for live dialer operations belongs in the review. Aged leads can help follow-up campaigns. They should not be priced like real-time calls.

Why Insurance Live Transfers Are Not One Product

The phrase “insurance live transfers” covers many markets. This article is narrower than the broader insurance lead generation category because it focuses on real-time calls.

A Medicare call is not the same as an auto insurance call. A final expense call is not the same as a business insurance call. A health insurance call has different rules from a home insurance call.

Here is the first rule:

Do not buy generic insurance transfers. Buy a clear insurance type.

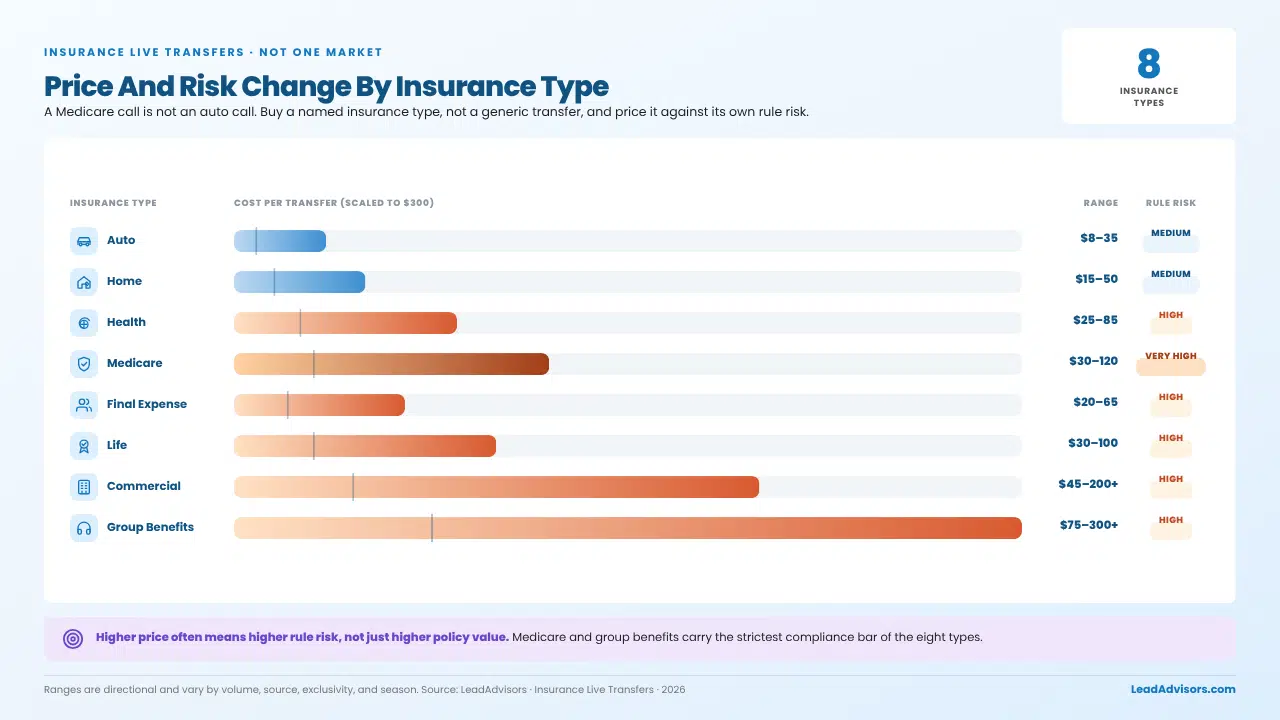

The main types include health, Medicare, final expense, burial insurance, life insurance, auto, home, P&C, business insurance, and group benefits.

Each type changes the script, checklist, price, rules, and agent assignment.

The Insurance Live Transfer Sub-Vertical Stack

Use this stack before buying live transfer insurance leads.

| Insurance Type | Typical Cost | What To Check | Rule Risk | Best Fit |

| Auto | $8–$35 | State, vehicle, coverage, driver profile | Medium | Fast quoting teams |

| Home | $15–$50 | State, property type, coverage | Medium | P&C agencies |

| Health | $25–$85 | State, age, income, coverage, enrollment fit | High | Licensed health teams |

| Medicare | $30–$120 | Age, Medicare status, plan interest, state | Very high | Medicare-trained agents |

| Final Expense | $20–$65 | Age, state, coverage need, health check | High | Senior-market agencies |

| Life | $30–$100 | Age, coverage amount, health, income | High | Life insurance agents |

| Commercial | $45–$200+ | Business type, revenue, employees | High | Business insurance teams |

| Group Benefits | $75–$300+ | Company size, employees, renewal date | High | Benefits agencies |

These ranges are a guide. Real pricing depends on call volume, source, lead quality, exclusivity, location, and season.

The same vertical logic applies to both mortgage and debt vertical live transfer operations.

It also applies to tax vertical live transfer operations and merchant cash advance live transfer operations.

The product changes, but the question stays the same: does the call match the buyer’s license, offer, agent, and rules?

Insurance Live Transfer Cost Benchmarks by Type

Cost per call is only the first number. Operators care about cost per new policy. That number links call price, close rate, policy value, and retention.

For buyers comparing financial markets, financial services lead generation provides useful context on lead sources and costs.

Auto, Home, and P&C Live Transfers

Auto insurance live transfers are often the lowest-cost insurance calls, usually $8 to $35 per transfer. These calls often come from people shopping for lower rates, replacing coverage, adding a car, or reacting to a price increase.

The vendor should check state, current coverage, vehicle details, driver profile, quote interest, consent, and call source. Auto buyers need speed. If the agent cannot provide a quote quickly, the call loses value. That same response-time issue sits behind speed-to-lead infrastructure in every live call program.

Home insurance live transfers usually cost $15 to $50 per transfer. These calls may come from homeowners, renters, refinance events, home purchases, or rate shoppers. They work best for P&C agencies with carrier access and bundle options.

If the buyer also runs mortgage campaigns, compare the numbers with mortgage refinance lead operations.

Then use the mortgage lead-generation methodology to compare lead sources and costs.

Health Insurance Live Transfers

Health insurance live transfers usually cost $25 to $85 per transfer. They need more checks because health insurance depends on age, income, state, current coverage, and enrollment rules.

CMS Marketplace guidance lists Acceptable Risk Controls for ACA, Medicaid, and Partner Entities with a March 2026 compliance date. That shows why health campaigns need stronger records than basic call campaigns.

Health campaigns should check state, age, household size, income range, current coverage, enrollment fit, consent, and product fit.

Weak checks create wasted calls. Strong checks help agents spend time on people they can actually help.

Medicare Live Transfers

Medicare live transfers are one of the highest-risk insurance call types. Typical pricing ranges from $30 to $120 per transfer.

CMS says its Medicare marketing guidelines reflect federal marketing requirements for Medicare Advantage and Prescription Drug Benefit rules under 42 CFR Parts 422 and 423. Medicare calls need more than a basic interest check.

The vendor should check Medicare eligibility, state, Part A and Part B status, current coverage, product interest, consent path, and agent license fit.

KFF’s 2026 Medicare Advantage enrollment analysis shows that UnitedHealth Group and Humana together account for 46% of Medicare Advantage enrollees nationwide in 2026. KFF also reports in its 2026 Medicare Advantage premiums and benefits analysis that 75% of Medicare Advantage prescription drug plan enrollees are in plans with no extra premium beyond the Part B premium.

For the rule definition, eCFR defines a third-party marketing organization as a group engaged in lead generation, marketing, sales, or enrollment work within the Medicare Advantage chain.

Medicare transfers should only go to agents trained on Medicare rules.

Final Expense, Burial, and Life Insurance Live Transfers

Final expense and burial insurance live transfers usually cost $20 to $65 per transfer. These calls often target older consumers seeking small life insurance policies to cover funeral, burial, or end-of-life costs.

The vendor should check age, state, coverage amount, current life insurance, basic health facts, and consent. Final expenses can close more easily than many other insurance types because the need is often clear. Senior-market campaigns still need careful scripts and rule checks.

Life insurance live transfers usually cost $30 to $100 per transfer. These include term life, whole life, and related products. Checks should include age, state, coverage amount, health profile, income, current coverage, consent, and source.

Life insurance transfers can work well when agents understand the underwriting process. If the agent cannot explain the next steps, the call can stall.

Commercial and Group Benefits Live Transfers

Commercial insurance transfers usually cost $45 to $200 or more per transfer. They cost more because the policy value can be higher, and the sales process takes longer.

The vendor should check business type, state, revenue range, employee count, current coverage, coverage need, and renewal timing. Commercial calls should go to business insurance specialists, not general personal-lines agents.

Group benefits transfers can cost $75 to $300 or more. They require company size, employee count, current benefits, renewal date, and decision-maker status.

Qualification Depth: Where ROI Actually Lives

Lead quality decides whether transfers become policies or wasted calls. Use the live transfer qualification framework to define what must happen before a call reaches the agent.

A cheap transfer can become expensive if the agency cannot close it. A higher-priced transfer can be a better deal if it has better checks.

Baseline checks confirm product interest, target state, willingness to speak with an agent, recorded consent, and lead source.

Standard-plus checks add product details: age, income, vehicle info, property info, current coverage, and basic fit. This helps route calls to the right licensed agent.

Deep checks add health details, money fit, current agent status, urgency, bundle interest, claim history, or business size.

Here is the math:

- A $25 basic transfer at a 5% close rate creates a $500 cost per new policy.

- A $65 deep-checked transfer at a 20% close rate creates a $325 cost per new policy.

The second call costs more upfront. It can still create better results.

If the program tracks appointments, compare the transfer set rate versus the show rate metrics against the close rate. A set call that never happens still costs money.

Compliance: TCPA, CMS, ACA, and State Licensing

Insurance live calls carry more risk than many other lead types. Review TCPA compliance for outbound operations before growing any phone campaign.

The buyer must check the provider’s consent process, call source, script, and routing rules.

The FCC’s consumer guidance on unwanted robocalls and texts points people to the National Do Not Call Registry and state do-not-call resources. That shows why teams need consent records and do-not-call checks.

This is not legal advice. Insurance agencies should review campaigns with a qualified lawyer.

TCPA and Consent

TCPA risk starts with consent. The FCC keeps updating robocall and text rules. For example, the FCC removed its one-to-one consent rule after a court decision nullified it in 2025. That matters because many articles still share old summaries.

Ask every provider for consent records. These should show how the person opted in, when consent was given, what message was shown, which seller was named, how opt-outs are handled, and whether recordings are saved.

Cheap calls with weak consent records can create risk beyond the lead budget.

Medicare, ACA, and Licensing Controls

Medicare calls need special care. CMS’s Contract Year 2026 Medicare Advantage and Part D final rule covers 2026 updates for Medicare Advantage and Part D. Medicare calls need trained agents, approved scripts, and clear records.

Health insurance transfers also need care. ACA marketplace enrollment depends on rules, timing, eligibility, and consent. CMS Marketplace guidance includes agent and broker resources, consumer consent requirements, and application review controls.

State licensing decides whether an agent can take the call. NIPR’s insurance licensing center helps producers apply, manage, renew, update, and verify licenses. NAIC’s Producer Database for licensing, appointment, and regulatory action data stores records from participating states.

Every provider should filter by state, product type, agent license, time zone, and transfer schedule.

Unit Economics: Cost Per New Policy Beats Cost Per Transfer

Live transfer prices can distract buyers. The cheaper call is not always the better call.

Use this formula first:

Cost per transfer ÷ close rate = cost per new policy

Examples:

- $22 auto transfer at 15% close rate = $147 cost per new policy

- $45 health transfer at 8% close rate = $563 cost per new policy

- $85 Medicare transfer at 15% close rate = $567 cost per new policy

- $35 final expense transfer at 22% close rate = $159 cost per new policy

- $65 deep-checked life transfer at 20% close rate = $325 cost per new policy

Then compare that number with policy value and retention. CMS explains in its Medicare agent and broker compensation guidance that Medicare agents and brokers often receive a first-year payment and about half as much in later years when a member stays enrolled or makes a like-plan change.

That shows why insurance ROI should not stop at the first sale. Retention matters.

Track these numbers by insurance type and vendor:

- Transfer volume

- Answer rate

- Missed transfer rate

- Qualified-call rate

- Close rate

- Bind rate

- Cost per new policy

- Policy value

- Retention

- Refund or dispute rate

- Compliance issue rate

Use call center operator metrics to separate activity reports from real results. Do not judge a provider after one day. Do not run blind for 90 days either. Use daily reports, weekly quality checks, and a 30- to 60-day pilot.

Closer Readiness: The Failure Point Buyers Underestimate

Many live transfer campaigns fail after the handoff. That is why training closers to receive warm transfers matters before the first test starts.

The provider sends a checked prospect. Then the agency misses the call, sends it to the wrong agent, or lets an untrained agent handle it.

Watch for these gaps:

- Agents cannot answer product questions.

- Agents lack a license in the prospect’s state.

- The agency has too few carrier options.

- Medicare agents do not know the rules.

- Life agents cannot explain the underwriting steps.

- Auto agents quote too slowly.

- Managers do not review recordings.

- Follow-up is weak after the first call.

Use mock call scripts for closer training to test readiness before paid calls go live. A readiness check should also include dialer technology selection if the team calls leads back.

Before buying, confirm that licensed agents are available. Test overflow routing. Prepare scripts. Train objections. Review rules. Check recordings. Use call notes and daily reports.

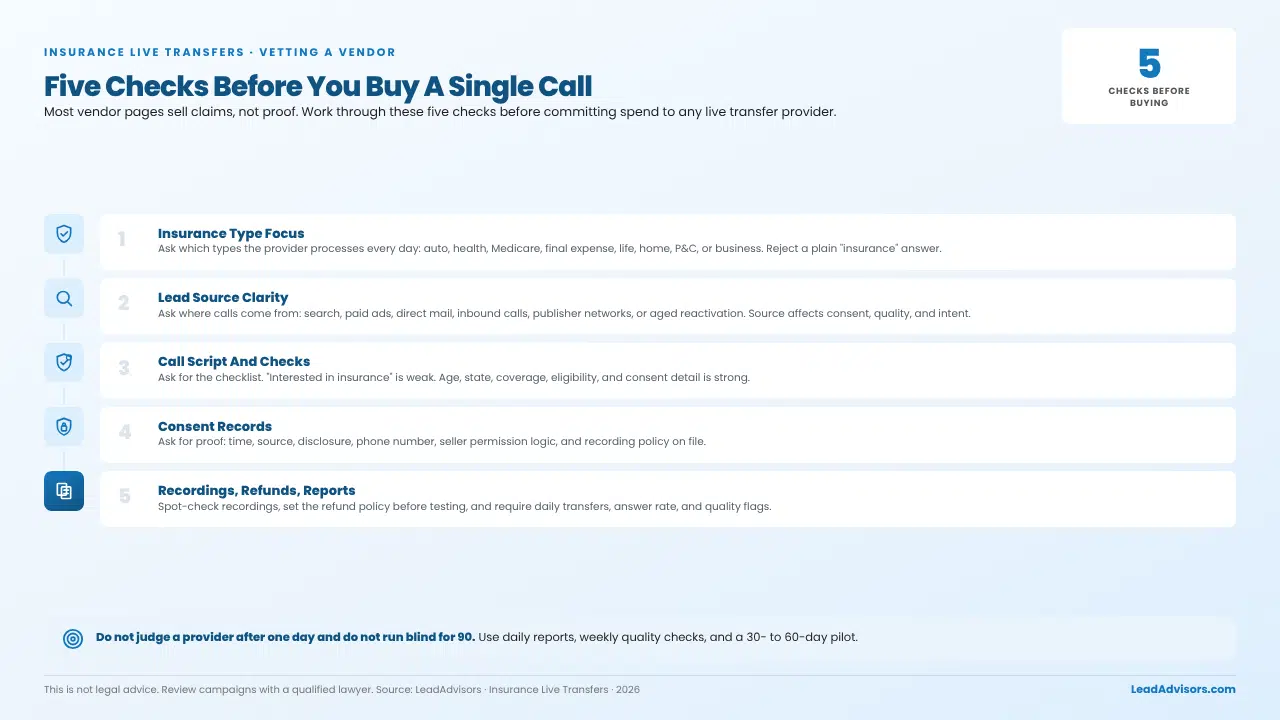

How to Evaluate an Insurance Live Transfer Provider

Many search results for this topic come from vendor pages. Buyers need a simple checklist that goes beyond sales claims.

For a broader view of sourcing, compare providers against the lead-generation vendor evaluation matrix.

Then check whether each provider fits the lead-generation services stack.

1. Insurance Type Focus

Ask which types of insurance the provider processes every day. Do not accept “insurance” as the full answer. Ask about auto, health, Medicare, final expense, life, home, P&C, and business calls.

The provider should know the price, checks, and rule differences for each type.

2. Lead Source Clarity

Ask where the calls come from. Sources may include search traffic, paid ads, direct mail, inbound calls, publisher networks, call center outreach, aged lead reactivation, or referral traffic.

The answer affects consent, quality, and intent. If the provider cannot explain sources, the buyer cannot judge risk.

3. Call Script and Checks

Ask for the call checklist. “Interested in insurance” is weak.

“Age 67, enrolled in Medicare Part A and B, lives in Texas, wants to compare Medicare Advantage options, and agreed to speak with a licensed agent” is stronger.

Clear checks improve routing and close rate. They also align the campaign with a contact-rate optimization methodology rather than simple volume reports.

4. Consent Records

Ask for proof of consent. The National Do Not Call Registry is run by the FTC, and buyers should confirm that call workflows account for federal and state do-not-call rules before launch.

At a minimum, the provider should record the time, source, disclosure, phone number, seller permission logic, and recording policy.

5. Recordings, Refunds, and Reports

Spot-check recordings to confirm that the person matched the rules, consent was clear, and routing was correct.

Set the refund policy before the test starts. Common reasons for disputes include the wrong state, the wrong product, a duplicate call, no consent, dead air, a disconnected call, an existing customer, an unqualified prospect, or an underage prospect.

Good providers report more than call count. Ask for daily transfers, call results, answer rate, quality flags, refunds, close-rate feedback, and source trends.

Insurance Live Transfers vs Internet Insurance Leads

Insurance agents often compare live transfers with internet leads. The right answer depends on the agency’s system.

Internet leads can work when the agency has fast follow-up and enough agents to chase leads. They usually cost less per lead but require more labor. When those leads come from inbound channels, inbound call center support becomes part of the sales system.

Live transfers cost more. But they reduce the contact problem because the person is already on the phone.

| Lead Type | Cost | Labor Needed | Contact Rate | Best Use |

| Internet Leads | Lower | High | Varies | Teams with strong follow-up |

| Aged Leads | Lowest | Very high | Low | Win-back campaigns |

| Shared Leads | Low to mid | High | Competitive | Low-cost tests |

| Warm Transfers | Mid to high | Medium | Higher | Trained sales teams |

| Live Transfers | Highest | Lower upfront | Highest | Ready agents with capacity |

Live transfers do not replace follow-up. They change where the work happens. The provider handles more pre-call work. The agency must handle the sales call and follow-up.

For teams running both live transfers and outbound calls, outbound dialing campaign operations should support the follow-up plan.

Common Mistakes That Destroy Insurance Live Transfer ROI

Most failures are easy to predict. Avoid these mistakes before spending serious money.

Buying Generic Insurance Transfers

Generic insurance calls create routing problems. A Medicare-only agency cannot use auto calls. A P&C agency may not handle final expenses. A health agency may not be licensed in the person’s state.

Choosing Based on Cost Per Transfer

Cheap calls can create costly policies. Always calculate the cost per new policy. Then compare it with policy value and retention.

Ignoring Compliance

Weak consent records create risk. This matters even more in Medicare, health insurance, and senior-market campaigns.

Missing Calls

Missed transfers burn the budget fast. The person is alive. The agent must answer. Build backup routing before the volume starts.

Undertraining Agents

Checked prospects still need strong agents. Train agents on product knowledge, objections, rules, and follow-up.

Skipping Recording Review

Vendor claims are not enough. Review recordings and compare them with call results.

Ending the Pilot Too Early

One week is rarely enough. Most campaigns need time to adjust. A 30- to 60-day test gives better data. Major rule issues should stop the test right away.

How LeadAdvisors Thinks About Insurance Live Transfers

LeadAdvisors views live transfers through an operator’s lens. The call is only one part of the system.

For a broader view of acquisition, connect this to the customer acquisition strategy framework.

For agencies comparing build versus partner models, the in-house vs. outsourced BPO comparison helps clarify where the operational work should live.

The full system includes lead source, consent, call script, routing, licensed agent coverage, QA review, reports, follow-up, and cost per new policy.

A live transfer program works when the agency integrates lead quality, rules, agent readiness, and reporting into a single model. That model is closest to BPO contact strategy operations when the agency needs managed calling, QA, and call reports.

Insurance needs extra care. Medicare, health, life, final expense, auto, home, and business lines each need different routing and checks.

Before scaling spend, map the current setup against the Insurance Live Transfer Sub-Vertical Stack. Then check consent depth, lead quality, and agent readiness. If those pieces are weak, more calls will not fix the system.