The refinance lead problem in 2026 is not supply.

Cash-out refis alone made up 41% of total refi activity in January 2026; that market exists. The problem is that most operators are running a single sourcing channel against a fractured buyer pool, then wondering why contact rates are soft and pull-through is weak.

Rate-and-term, cash-out, and debt consolidation are three different sales with three different urgency drivers. Treat them the same, and you pay three times over: wasted CPL, wasted LO time, and funded loans that should have been yours.

What Changed About Refinance Leads Since 2022 (and What It Means for Your Refi Book)

Refi got hit harder than purchase when rates moved. The bigger change is that refi demand fractured into distinct pools, and the conversion cycle became more sensitive to operational execution.

Shift 1: The refi buyer pool fractured by rate

Refi prospects in 2026 typically fall into three pools:

- Rate-and-term: they move when rate-improvement math works

- Cash-out: they move when accessing home equity is the driver

- Debt consolidation: they move when high revolving debt is the driver

That last pool is not theoretical. The Federal Reserve’s G.19 Consumer Credit release has continued to show periods of rapid growth in revolving credit in 2026, which supports the view that debt-driven refi demand persists even when rates are not “low.”

Shift 2: Aggregator lead quality became more variable

Aggregators were built to expand the pool of rate improvements. When the pool shrinks, lead quality variance increases. Operators buying mortgage refinance leads from aggregators need stricter intake filters than they needed earlier in the cycle.

Shift 3: Cash-out and debt consolidation became the volume drivers

For many operators, cash-out and debt consolidation have carried refi volume because the buyer driver is equity or debt pressure, not a headline rate.

FHFA’s Foreclosure Prevention, Refinance, and Federal Property Manager’s Report shows that in January 2026, the share of cash-out refinances was 41.0% of total refinance activity. That is a clear signal that “cash-out refinance leads” are not a niche edge case. They are a major slice of refi activity.

Shift 4: Refi urgency shrunk

In peak refi cycles, urgency was structural. In 2026, urgency is buyer-specific. Cash-out prospects can move fast. Debt consolidation prospects often move when monthly payments break. Rate-and-term prospects wait.

This is why refi sequencing must be longer than purchase sequencing.

Shift 5: Compliance pressure raised the bar on lead buying

Lead buying in mortgage is under sustained regulatory pressure. Do not treat vendor consent language as a detail.

If you want an authoritative view of the current federal posture on consent rules, use the FCC order postponing the effective date of the one-to-one consent rule as a reference point. Coordinate with compliance counsel for your specific program.

Operator filter: In 2026, the best refinance mortgage leads are the ones your compliance and intake process can actually work at scale without creating downstream risk.

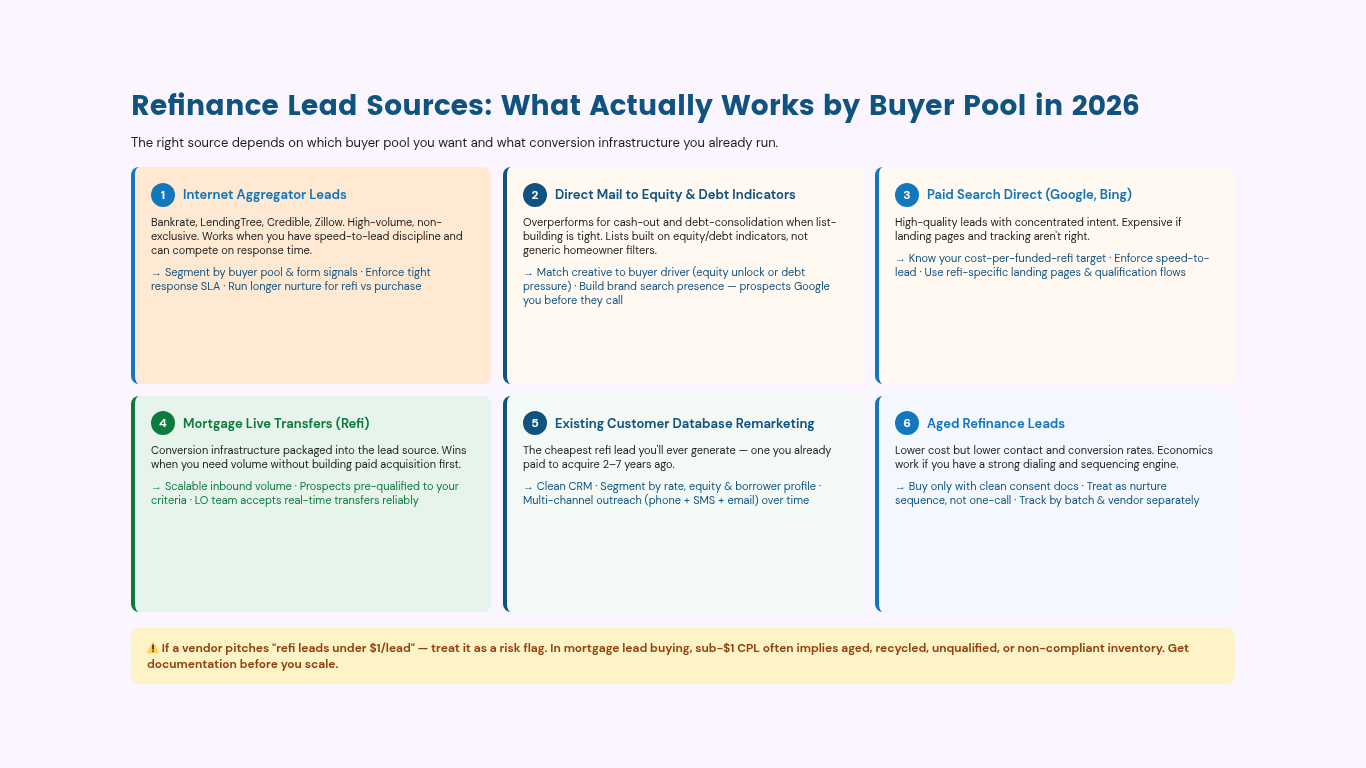

Refinance Lead Sources: What Actually Works by Buyer Pool in 2026

The right refinance lead source depends on which buyer pool you want and what conversion infrastructure you already run.

Source 1: Internet aggregator refinance leads (Bankrate, LendingTree, Credible, Zillow)

Aggregators remain the largest-volume source for many operators. They capture high-intent queries, then sell leads (often non-exclusive) to multiple lenders.

When it works

- You have speed-to-lead discipline

- You can compete on response time, trust, and follow-up

- You have the capacity for non-exclusive lead competition

How to use it in 2026

- Segment your buy by buyer pool and lead form signals

- Enforce a tight response SLA

- Run a longer nurture sequence for refi than you run for purchase

Source 2: Direct mail to home equity and debt indicators

Direct mail continues to overperform for cash-out and debt-consolidation refis when your list-building is tight.

What makes mail work

- Lists built on equity and debt indicators, not generic homeowner filters

- Creative that matches the buyer driver (accessing home equity or debt pressure)

- Brand search presence (prospects Google you before they call)

If you run mail, you also need brand authority. That is why direct mail and branded search are linked.

Source 3: Paid search direct (Google Ads, Bing Ads)

Paid search can generate high-quality mortgage refinance leads because the buyer’s intent is highly concentrated. It is also expensive if you do not have landing pages and tracking right.

When it works

- You know your cost per funded refi target

- You can enforce speed-to-lead

- You have refi-specific landing pages and qualification flows

Source 4: Mortgage live transfers (refi-specific)

Mortgage live transfers are the “conversion infrastructure packaged into the lead source.” They can win when you need volume without building paid acquisition systems first.

Use this source when:

- You need a scalable inbound volume

- You want prospects pre-qualified against your criteria

- Your LO team can accept real-time transfers reliably

Source 5: Existing customer database remarketing

The cheapest refinance lead you will ever generate is the one you already paid to acquire two to seven years ago.

This channel works when:

- Your CRM is clean

- You can segment by rate, equity, and borrower profile

- You run multi-channel outreach (phone + SMS + email) over time

Source 6: Aged refinance leads

Aged refinance leads are attractive because they cost less. They also produce lower contact and conversion rates. The economics can still work if you have a strong dialing and sequencing engine.

How to make aged refi leads work

- Buy only when consent and sourcing documentation are clean

- Treat them as a nurture sequence problem, not a “one-call” problem

- Track performance by batch and vendor. Do not blend into one KPI.

Important: If a vendor pitches “mortgage refinance leads under $1 per lead,” treat it as a risk flag, not a win. A CPL under $1 is not impossible in marketing. In mortgage lead buying, it often implies aged, recycled, unqualified, or non-compliant inventory. You need documentation before you scale.

The Conversion Infrastructure That Determines Whether Refinance Leads Fund Loans

Here’s the 2026 reality: refinance doesn’t reward “good leads.” It rewards the operator who can respond fast, run a longer sequence, and qualify tightly while borrowers shop.

If your conversion layer isn’t built for that cycle, you’ll keep paying for volume that doesn’t fund — especially when rates move and lead to competition spikes.

Refi is more conversion-sensitive than purchase in 2026 because urgency is lower and shopping behavior is higher.

Component 1: Sub-five-minute speed-to-lead with rate-improvement math ready at first contact

Speed-to-lead is still the simplest lever. But refi adds a requirement. When the borrower answers, your LO must be ready to talk numbers.

Build:

- Instant routing

- Rate scenario pre-work (as much as your compliance posture allows)

- A first-call script that moves to the next step without overpromising

Component 2: Multi-channel sequencing built for refi timing

For example, by implementing our proprietary sequencing model, one client increased their contact rates by 150% within the first 30 days.

Purchase sequences often die too early for refi.

A practical refi sequencing pattern:

- Days 0–14: 7 touches across phone + SMS + voicemail + email

- Days 15–60: 1 touch every 7–14 days

- Days 61–90: re-engagement tied to rate movement events and borrower triggers

Component 3: Branded search and rate transparency

Refi prospects compare. They Google. They check reviews. They ask peers.

If your brand results are weak, your CPL is not the problem. Your trust layer is.

Component 4: Refi-specific qualification and documentation

Refi underwriting realities differ from purchase underwriting.

At intake, document and enforce:

- current loan balance range

- current rate (if available)

- occupancy type

- credit score band

- loan size minimum

- state constraints and licensing coverage

- refi type (rate-term, cash-out, consolidation)

This is what prevents your LO team from locking files that do not pull through.

Refinance lead generation benchmarks (2026 operator ranges)

Benchmarks move fast. Use these as ranges and validate against your own program and current vendor pricing before scaling.

To anchor macro context, use forecast sources rather than “vibes.”

- Fannie Mae ESR projected refinance share rising from 26% (2025) to 35% (2026) in its September 2025 outlook.

- MBA forecasted 2026 refinance originations at $737B in its October 2025 forecast release.

Cost benchmarks (refi lead cost)

- Aggregator rate-and-term refinance leads: typically lower than direct search leads, but this depends on exclusivity and competition.

- Direct paid search refi: highest CPL, highest intent

- Direct mail response cost: depends on list, creative, and brand trust

- Live transfers: higher cost per transfer, higher conversion probability

- Aged refinance leads: lowest CPL, lowest contact rates

Contact rate benchmarks (refi-specific)

Contact rate is an infrastructure metric. It moves with speed-to-lead and sequencing, not with “lead quality” alone.

Track contact rate separately for:

- aggregator

- paid search

- live transfers (near 100% by definition)

- aged leads

- database remarketing

Conversion benchmarks (lead to funded refi)

The best benchmark is not lead-to-funded in isolation.

Track: funded refi per qualified lead by source.

That number tells you:

- whether the source produces fundable borrowers

- whether your conversion engine is working

- where to reallocate the budget

Common refinance lead generation mistakes

Mistake 1: Treating all refi prospects as one pool

Rate-and-term and debt consolidation are not the same sale. Segment.

Mistake 2: Giving up on the sequence too early

Refi needs a longer follow-up. You do not lose the deal at touch seven. You lose it when you stop.

Mistake 3: No numbers ready on the first call

If you cannot credibly answer basic rate and payment questions, the borrower shops to someone who can.

Mistake 4: Ignoring the existing database

Your CRM is a refi lead source. Treat it like one.

Mistake 5: Buying cheap inventory without proof

Cheap refinance mortgage leads are only “cheap” if they fund without compliance problems. Audit first, then scale.

Build in-house refi acquisition vs outsource to a managed partner

Build in-house when

- Your LO team is refi-specialized

- Your database remarketing is the core channel

- You have a real edge in pricing or market coverage

Outsource when

- You need a scalable volume from non-database sources

- Your gap is infrastructure (routing, sequencing, QA, reporting)

- You need speed to launch without a 6–9 month build

LeadAdvisors helps mortgage operators turn refinance lead volume into funded loans by building the conversion layer: sub‑5‑minute routing, refi-specific qualification, multi-touch sequencing, and compliance-ready lead-intake documentation. We’re not a “lead source” — we’re the system that makes your sources perform in a slower, shop-heavy refi cycle. If you already have channels working, we can help improve pull-through. If you’re rebuilding from scratch, we help you launch without a 6–9-month internal build.

The hybrid model (common)

- In-house: LO team + database + underwriting alignment

- Outsourced: speed-to-lead engine + multi-touch sequencing + compliance documentation workflows + source conversion operations