We work with mid-market mortgage operators who run 40 loan officers across a few states. In 2022, many teams could buy leads, follow up, and still hit goals.

In 2026, the math broke.

CPL is up 60 percent. Contact rate is stuck at 11 percent. Funded loans per LO are down by half.

The team did not get worse. The market changed. Refi dropped. The buyer pool shrank. Vendors kept selling the same lead products. However, the unit economics under those products changed.

So the reflex shows up fast. Buy more leads. Switch vendors. Pay for “exclusive.”

That move often makes the problem worse. It increases spending without fixing conversion.

We have seen the pattern firsthand. For one 45-LO team, we lifted the contact rate from 11% to 28% in 60 days by tightening speed-to-lead and multi-channel follow-up.

Mortgage lead generation in 2026 is not just a sourcing problem. It is a conversion infrastructure problem.

In this post, you will get:

- The lead sources that still work in 2026

- Benchmarks you can use to spot what is broken

- The conversion infrastructure that turns leads into funded loans

What Is Mortgage Lead Generation, and What’s Actually Changed Since 2022?

Mortgage lead generation means finding prospects with real mortgage intent and routing them to a loan officer who can qualify and close. Intent can be purchase, refinance, cash-out, HELOC, or reverse.

The mechanics are not new. The economics are.

Here are five shifts that broke the old playbook.

Shift 1 – Rate environment compressed the buyer pool

Rates rose. Many buyers no longer qualify for today’s payment. As a result, lead quality declined across many sources, even as lead volume remained flat.

Shift 2 – Lead vendor margins shifted

When refi demand fell, vendors adjusted pricing. Therefore, many teams saw higher CPL on purchase leads and even higher CPL on refi leads.

Shift 3 – Contact rate compressed

Prospects answer fewer calls. They also shop with more lenders. So one call and one email no longer work.

Shift 4 – Compliance got stricter

Consent rules got tighter. As a result, operators need clearer consent records tied to their company. If you cannot prove consent, you carry real legal and operational risk.

Shift 5 – Branded search became conversion infrastructure

After a call or a mail piece, prospects Google the company name. If the search results look thin, the lead cools quickly.

Operators who adjusted to all five shifts can still fund loans at workable economics. Operators who did not see the shift often blame lead quality, even when the real issue is conversion.

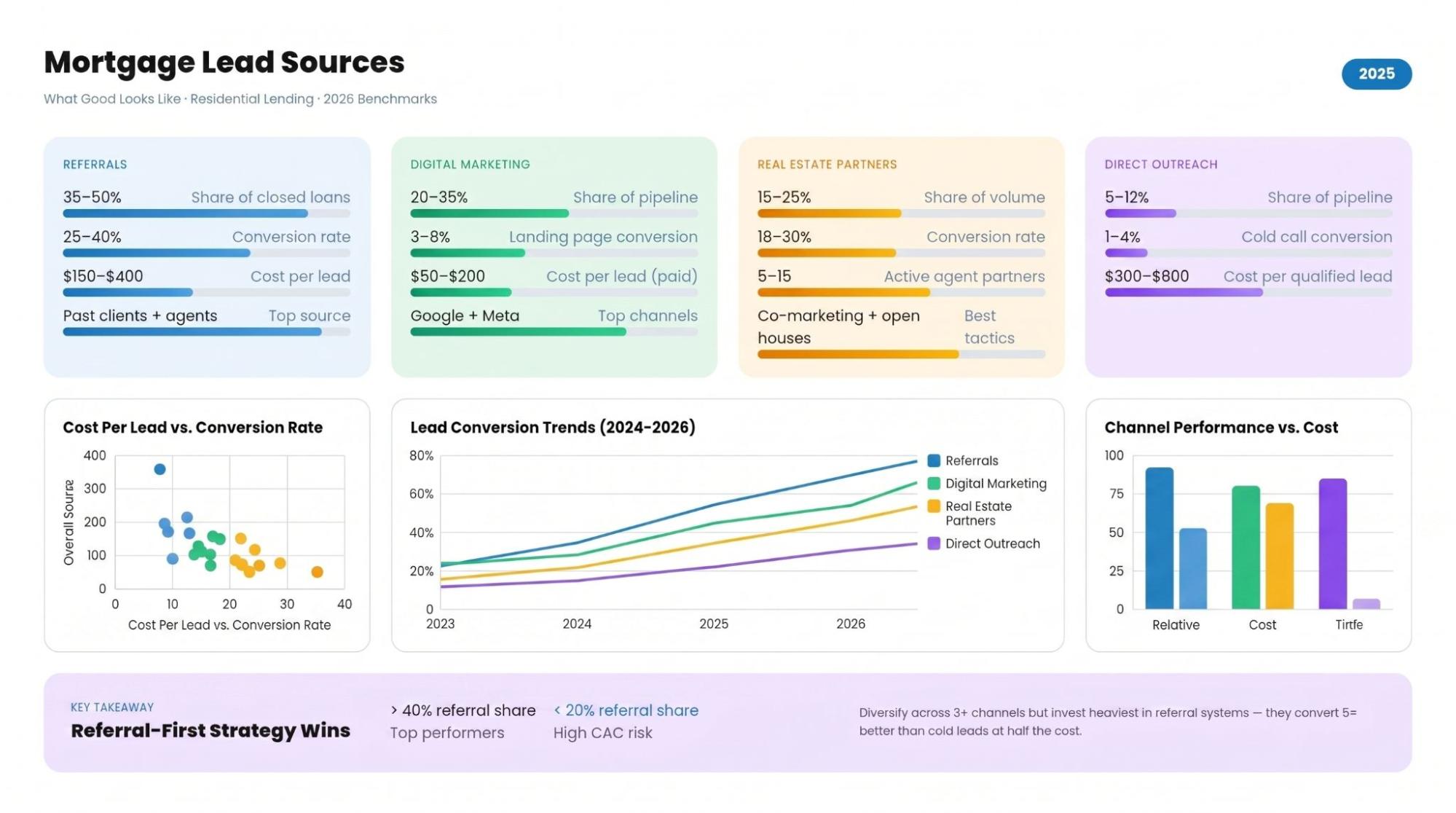

Mortgage Lead Sources – What Actually Works in 2026

The right mix depends on your scale, market, and follow-up engine. Still, six sources account for most of the volume in 2026. Most operators run three to five of them.

Source 1 – Internet aggregator leads (Bankrate, LendingTree, Zillow, NerdWallet, Credible)

This is the biggest volume source for many operators. Aggregators capture intent and sell leads. Many are not exclusive.

CPL often runs:

- Purchase: 20 to 80 dollars

- Refi: 15 to 60 dollars

Without fast follow-up, the contact rate often sits at 8 to 15 percent. With a sub-five-minute response plus multi-channel follow-up, it can reach 25 to 40 percent.

In other words, the leads can work. The infrastructure decides if they fund loans.

Operator filter: best fit for teams with a strong contact-rate engine and 15 plus LOs.

Source 2 – Direct mail with strong brand presence

Direct mail can still perform for purchase and refi. It often works best in higher-credit segments.

Typical ranges:

- Cost per piece: 0.45 to 0.85 dollars

- Response rate: 0.5 to 1.5 percent

However, mail only works if trust closes fast. Many prospects will Google your name after they read the piece. If they do not see credible results, you lose them.

That is why direct mail performs best when your brand holds up on Google. The Direct Mail Brand Reputation Stack breaks down what to build so mail responders trust what they find.

Operator filter: best fit for teams with 20K plus monthly mail budget and strong branded search.

Source 3 – Paid search direct (Google Ads, Bing Ads)

Paid search can produce high-intent leads. It also has the highest CPL.

CPL often runs $80 to $300, depending on the market and loan type.

These leads can convert well. But only if you have:

- A landing page built to convert

- Tracking that shows what is working

- Follow-up that starts within five minutes

If paid search is part of your mix, PPC management is where tracking, landing pages, and follow-up speed usually determine whether CPL turns into funded loans.

Operator filter: best fit for teams that can keep the cost per funded loan under $5,000.

Source 4 – SEO and content-driven inbound

SEO leads often convert well because the prospect found you on purpose. Once it works, the cost per lead can stay low.

The tradeoff is time. In competitive markets, SEO often takes 12 to 24 months to drive steady volume.

If you need stronger trust signals fast, brand authority is the lever that improves what prospects see when they research your name.

Operator filter: best for teams with an 18+ month runway.

Source 5 – Realtor partnerships and referral networks

Realtor referrals can be the best source of purchase leads. The lead often comes pre-screened.

The “cost” is not CPL. It is relationship time. That includes co-marketing, events, and lead-share plans.

Operator filter: best fit for teams that can build and keep partner relationships.

Source 6 – Mortgage live transfers

Live transfers are real-time calls with pre-qualified prospects. Pricing varies by how deep the screening is and how exclusive the transfer is.

CPL often runs $65 to $200 per transfer.

Because the prospect is already on the phone, conversion rates can be higher than for standard form-fill leads.

That is why many operators use mortgage live transfers when they need higher-intent conversations fast.

Operator filter: best fit for teams that need volume now and have a clean intake process.

Diversification matters. In many mid-market operations, single-source dependency is the most common failure mode. It also makes you vulnerable to a single vendor’s pricing changes.

The Conversion Infrastructure That Determines Whether Mortgage Leads Produce Loans

Lead source matters. However, conversion infrastructure matters more.

If your follow-up engine is weak, “better leads” will not save the math. You will pay more for the same outcome.

Four components tend to separate funded-loan operators from activity-only operators.

Component 1 – Speed-to-lead under five minutes, multi-channel

Recent lead-response-time findings and benchmarks: fast response lifts contact rate. Slow response kills it.

Many teams miss the five-minute window. They hit 45 minutes because the lead sits in a queue.

The fix is not just asking LOs to “call faster.” Instead, build an engine in front of the LO that:

- Calls, texts, and emails right away

- Confirms intent and basic fit

- Routes only engaged prospects to the LO

If your first response is not happening inside five minutes, start with speed-to-lead because it often lifts contact rate without changing your lead sources.

Component 2 – Multi-channel follow-up across at least seven touches over 10 to 14 days

Mortgage prospects shop. They compare lenders. They pause. Then they come back.

So you need a sequence, not one call.

A simple working pattern:

- Day 1: phone plus voicemail, then email

- Day 2: SMS

- Day 4: phone

- Day 6: email

- Day 8: phone

- Day 10: final email

This is not “more spam.” It is the cadence that reaches people when they are ready.

Component 3 – Branded search presence that closes the trust loop

Prospects research you before they call back.

If search results look weak, trust drops in minutes. If results look strong, the lead warms up.

This is why branded credibility matters. It supports every other channel.

This is also why brand trust matters. Brand authority and the Direct Mail Brand Reputation Stack both shape what prospects see when they look you up.

Component 4 – Compliance documentation that scales with volume

If you buy leads across markets, you need compliance that you can audit. That includes consent records, suppression logic, and calling-window controls.

If you cannot show the trail, you carry the risk. Also, risk does not scale linearly. It compounds.

If you are scaling outbound and buying leads across channels, TCPA compliance for high-volume outbound calling is worth reviewing before volume increases.

Operators who built these systems early did not have to rebuild when the market shifted. Operators who did not are now building while CPL rises.

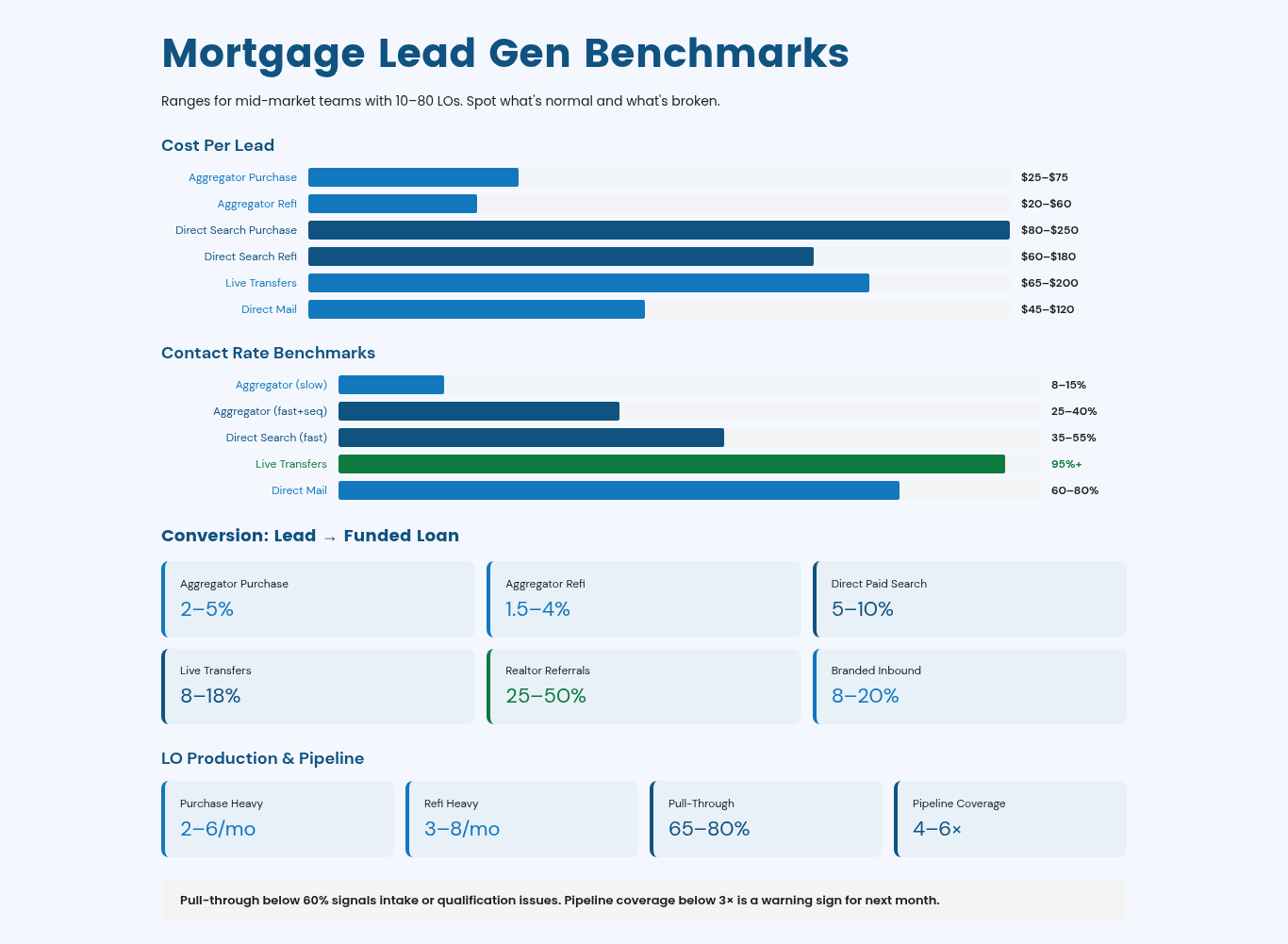

Mortgage Lead Generation Benchmarks

Benchmarks vary by market and loan type. Still, these ranges can help you spot what is normal and what is broken for mid-market teams with 10 to 80 LOs.

Cost benchmarks per lead

- Aggregator purchase leads: 25 to 75 dollars

- Aggregator refi leads: 20 to 60 dollars

- Direct paid search purchase: 80 to 250 dollars

- Direct paid search refi: 60 to 180 dollars

- Live transfers: 65 to 200 dollars per transfer

- Direct mail response cost: 45 to 120 dollars per response

Contact rate benchmarks

- Aggregator leads with slow response: 8 to 15 percent

- Aggregator leads with fast response and sequence: 25 to 40 percent

- Direct paid search with fast response: 35 to 55 percent

- Live transfers: 95 percent plus by definition

- Direct mail responders: 60 to 80 percent

Conversion benchmarks (lead to funded loan)

- Aggregator purchase: 2 to 5 percent

- Aggregator refi: 1.5 to 4 percent

- Direct paid search: 5 to 10 percent

- Live transfers: 8 to 18 percent

- Realtor referrals: 25 to 50 percent

- Branded inbound: 8 to 20 percent

Loan officer production benchmarks

A common funded-loans-per-LO range is:

- Purchase heavy: 2 to 6 per month

- Refi heavy in favorable windows: 3 to 8 per month

The average loan amount can swing by market. Pull-through often runs 65 to 80 percent in strong ops. A score below 60 percent can signal issues with intake or qualification.

Pipeline coverage benchmark

Pipeline value divided by monthly funded production often runs 4x to 6x in strong ops. Below 3x is a warning sign for next month.

Common Mortgage Lead Generation Mistakes

These mistakes show up in underperforming teams. They also hide in plain sight.

Mistake 1 – Single-source dependency on the aggregator leads

If one source supplies 80 percent of your leads, one pricing change can break you. Diversify across three to five sources to keep unit economics stable.

Mistake 2 – Treating speed-to-lead as optional

Five minutes is not a nice-to-have. It is a conversion lever. If you miss it, you lose value you cannot buy back.

Mistake 3 – Phone-only follow-up

Some prospects will not pick up. However, they may respond to a text or an email. Use phone, SMS, and email in one coordinated sequence.

Mistake 4 – No branded search presence

If you spend big on leads but look invisible on search, you leak conversions. Prospects research you. They decide fast.

Mistake 5 – No documented qualification criteria

When each LO qualifies differently, conversion becomes random. Write the criteria down. Train it. Enforce it.

In-House vs Outsourced Mortgage Lead Generation Operations

Build vs buy depends on scale and on what is broken right now. Use this simple filter.

Build in-house when:

- You have 50-plus LOs and can support fixed headcount for marketing ops and systems

- Lead acquisition is your moat, such as partner networks you control

- You have runway for SEO and content to compound over 12 to 24 months

Outsource when:

- Speed-to-lead is the gap, and you need to lift fast

- Compliance systems are the gap, and you need auditable processes

- Branded search is the gap, and you need credibility sooner than an internal build allows

The hybrid model

For many mid-market teams, the best answer is mixed. Keep strategy and partner channels in-house. Outsource the systems that run best as managed infrastructure.

If you are weighing build vs buy, lead generation outsourcing covers when a managed system is faster than hiring and building internally.

Frequently Asked Questions

What does mortgage lead generation cost in 2026?

What does mortgage lead generation cost in 2026?

Cost varies by source. Aggregator leads often run $20 to $80. Direct paid search often runs $80 to $300. Direct mail response cost can run from 45 to 120 dollars. Live transfers often run 65 to 200 dollars. However, cost per lead is not the final metric. Cost per funded loan is.

What is the best source of mortgage leads?

There is no single best source. The best source depends on your team size, market, and follow-up engine. Therefore, most strong operators run three to five channels instead of one.

How long does it take to generate mortgage leads through SEO?

In many competitive markets, SEO can take 12 to 24 months to produce steady volume. However, branded content can lift branded search sooner. If you need leads in under six months, start with paid channels and build SEO in parallel.

What is a good contact rate for mortgage leads?

For aggregator leads, 8 to 15 percent is common with slow response rates. With sub-five-minute response and a real sequence, 25 to 40 percent is common. In most cases, response time and cadence matter more than “lead quality.”

How does consent affect mortgage lead buying?

Consent must be clear and tied to the company doing the outreach. If consent is vague, you take on risk and may see lower conversion rates. Treat consent records like core infrastructure.

What does mortgage lead generation cost in 2026?

Cost varies by source. Aggregator leads often run $20 to $80. Direct paid search often runs $80 to $300. Direct mail response cost can run from 45 to 120 dollars. Live transfers often run 65 to 200 dollars. However, cost per lead is not the final metric. Cost per funded loan is.

There is no single best source. The best source depends on your team size, market, and follow-up engine. Therefore, most strong operators run three to five channels instead of one.

In many competitive markets, SEO can take 12 to 24 months to produce steady volume. However, branded content can lift branded search sooner. If you need leads in under six months, start with paid channels and build SEO in parallel.

For aggregator leads, 8 to 15 percent is common with slow response rates. With sub-five-minute response and a real sequence, 25 to 40 percent is common. In most cases, response time and cadence matter more than “lead quality.”

Consent must be clear and tied to the company doing the outreach. If consent is vague, you take on risk and may see lower conversion rates. Treat consent records like core infrastructure.

Conclusion

In 2026, the problem is rarely “we need more leads.” More often, the leads you already buy do not turn into conversations or funded loans quickly enough.

So we focus on the system.

Build infrastructure that lifts every channel:

- Respond in under five minutes using phone, SMS, and email

- Run seven or more touches across 10 to 14 days

- Tighten branded search so trust closes when prospects research you

- Keep consent and compliance records you can audit

Some teams will build this in-house. Others will outsource it. Most will run a hybrid.

If you want a clear plan for your own operation, start here: Get a mortgage lead generation audit.