Insurance lead generation is the process by which agents find and quote in-market buyers. The work spans eight channels. Each one fits a different vertical and a different buyer.

The math is not the same in every line. Auto looks one way. Health looks different. Life and final expense look different again. Cost per lead is the wrong thing to chase. Contact rate, qualified rate, and close rate are what move the margin.

The U.S. insurance industry employed three million workers in 2024. Combined ratios continue to improve through 2025 and 2026. That data comes from the Triple-I-Milliman P/C profitability report. Demand is large. The real bottleneck is the system that turns leads into calls and calls into policies.

This guide breaks down the four retail verticals. It shares 2026 CPL benchmarks. It walks through TCPA after the rule was vacated. And it lays out the contact rate framework that decides if bought leads pay off.

Quick Answer: What Is Insurance Lead Generation in 2026?

Insurance lead generation is the process of identifying prospects and routing them to a licensed agent. Eight channels make it work. They are shared aggregator leads, exclusive internet leads, live transfers, direct mail, paid search, social lead forms, SEO, and referrals.

The lead’s vertical, source, and exclusivity set its rates. The buyer’s speed, cadence, and channel mix decide if those rates show up. Together, they drive cost per issued policy.

Three things shifted between 2024 and 2026.

- The Eleventh Circuit vacated the FCC’s one-to-one consent rule in January 2025. It was formally removed from FCC rules in July 2025. See the FCC’s announcement and the Congressional Research Service’s report on unwanted robocalls. The rule is gone. TCPA, state AG action, and class action risk are not.

- Insurance and healthcare ranked second in 2025 FCC robocall complaints. They accounted for 11 percent of the total volume, per the FCC’s 2025 top-five robocall scam report. Trust in cold outreach is low.

- The FTC’s 2025 settlement with Assurance IQ and MediaAlpha hit $145 million. It reset the bar for health insurance lead generation. Lead quality and disclosure are now active targets rather than guidelines.

Agencies that win in 2026 will adapt to all three at once.

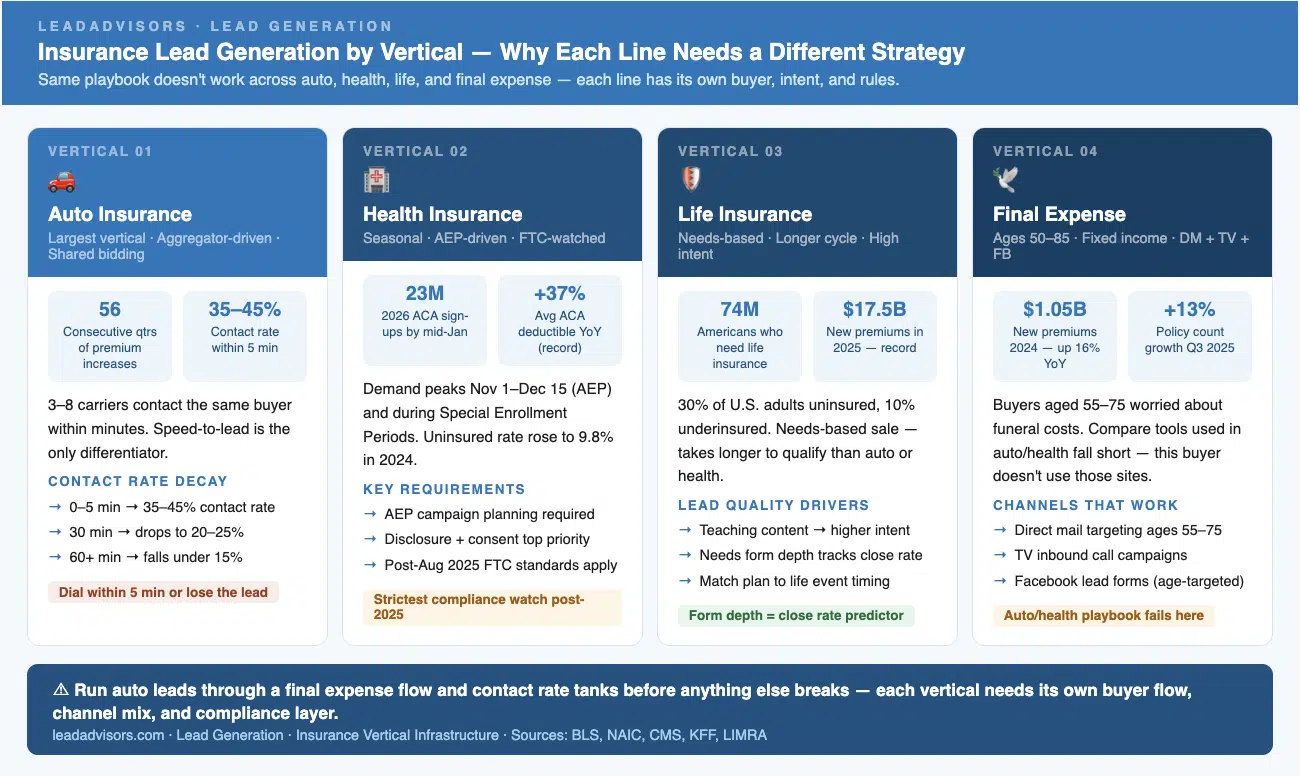

Insurance Lead Generation by Vertical: Why Each Line Needs a Different Strategy

The same playbook does not work across auto, health, life, and final expense. Each line has its own buyer, its own intent, and its own rules. Run auto leads through a final expense flow, and the contact rate will tank before anything else can break.

Auto Insurance Lead Generation

Auto is the largest vertical. Aggregator traffic drives most lead supply. The defining trait is shared bidding. Three to eight carriers contact the same buyer within minutes.

The Bureau of Labor Statistics CPI release shows the motor vehicle insurance index continued to rise in April 2026. The NAIC 2025 Mid-Year P&C Analysis Report shows commercial auto premiums rose 8.8 percent in Q2 2025. That is the 56th straight quarter of increases. Premiums are at record highs. The market is large for any carrier that can move fast.

Contact rate within the first five minutes drives auto-lead value. At five minutes, contact rates hit 35 to 45 percent. At 30 minutes, they drop to 20-25%. After 60 minutes, they fall under 15 percent.

Health Insurance Lead Generation

Health is seasonal. Demand peaks in the Annual Enrollment Period (November 1 to December 15). It also rises during Special Enrollment Periods after qualifying life events.

The CMS Marketplace Open Enrollment National Snapshot 2026 reports 23.0 million sign-ups for 2026 ACA coverage by mid-January. That included 3.4 million new enrollees. The KFF 2026 Marketplace report shows average ACA deductibles jumped 37 percent to a record $3,786 in 2026. That is the steepest one-year jump on record. The KFF uninsured population data show that the uninsured rate reached 9.8 percent in 2024. That is the first rise since 2019. Shoppers are active. The market is growing.

Health faces the strictest watch after the August 2025 FTC action. Disclosure and consent docs are now top priorities.

Life Insurance Lead Generation

Life is a needs-based sale. It takes longer to qualify than auto or health. The 2025 LIMRA Insurance Barometer Study says 74 million Americans need life insurance. Another 25 million say they need more than they have. That gap is 30 percent of U.S. adults with no coverage, plus 10 percent underinsured.

LIMRA’s 2026 release shows U.S. individual life insurance hit $17.5 billion in new premiums in 2025. That is a sales record. Demand is real. The job is matching the right plan to the right life event at the right time.

Life leads from teaching content or needs forms have a higher intent than leads from generic quote tools. Form depth (how many specific questions a buyer answers) tracks closely with close rate.

Final Expense Lead Generation

Final expense targets adults 50 to 85 on fixed incomes. These buyers worry about funeral costs for their families. The 2024 LIMRA-Life Insurers Council Final Expense Survey shows new premiums hit $1.05 billion. That is up 16 percent year over year. The 28 reporting carriers sold 1.06 million policies.

LIMRA’s December 2025 third-quarter release shows that final expense continued to lead whole life growth through Q3 2025. Whole life new premium rose 9 percent. Policy count rose 13 percent.

Final expense needs sharp targeting. Direct mail, TV inbound calls, and Facebook lead forms aimed at ages 55 to 75 work best. Compare tools that work for auto and health fall short here. The typical final expense buyer does not use those sites.

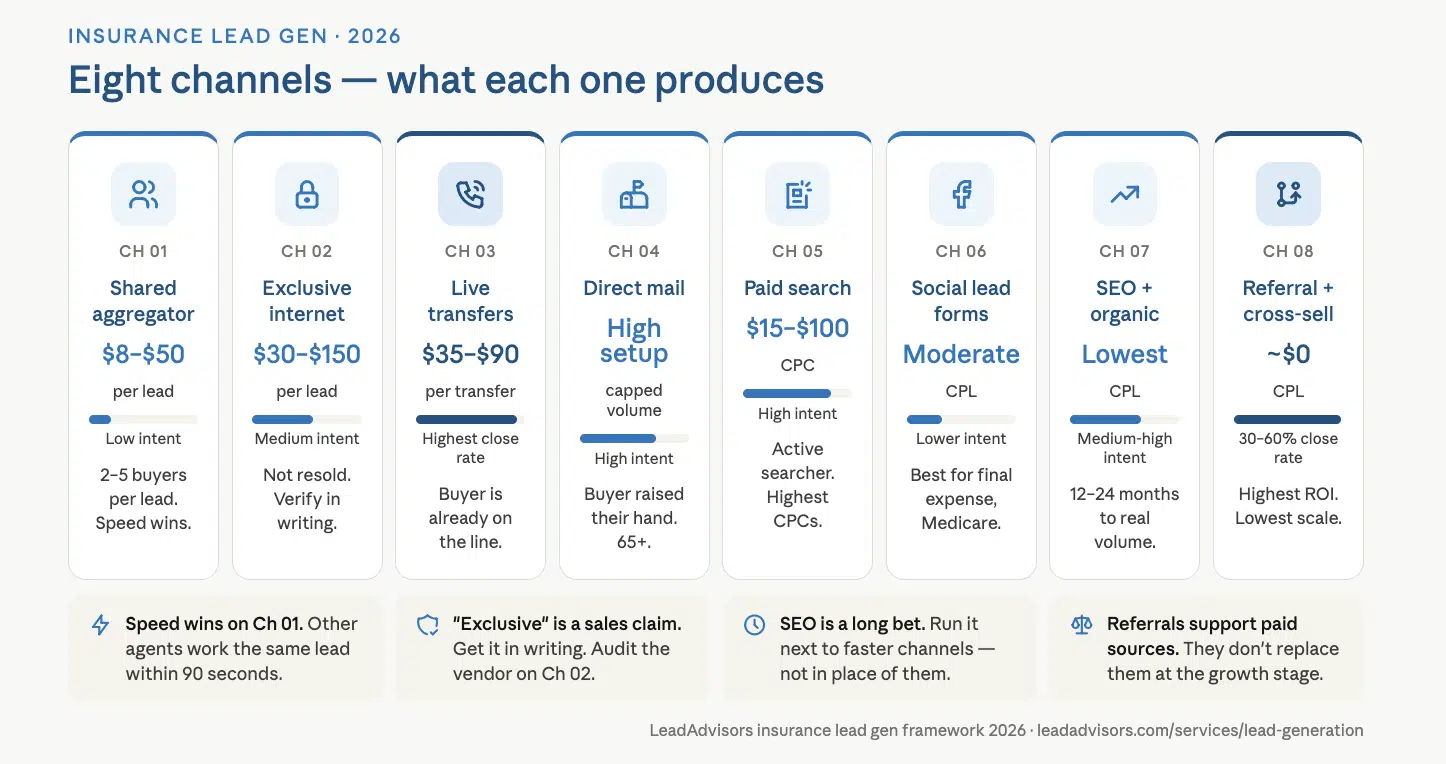

The Eight Insurance Lead Generation Channels: What Each One Produces

These eight sources make up the mix that works in 2026. They are not swappable. Each one fits a few verticals and a few operator types.

Channel 1: Shared Aggregator Leads

Buyers submit info on comparison sites. The lead goes to two to five buyers at once. Pricing is the lowest across all channels.

Volume is high. Auto shared leads run $8 to $25. Health runs $15 to $40. Life runs $20 to $50. Final expense runs $10 to $30.

The contact rate problem is built in. Other agencies work the same lead within 90 seconds. The first agent to reach the buyer wins most of the quoting shots.

Channel 2: Exclusive Internet Leads

One buyer gets the lead. It is not resold. Exclusive leads come from owned landing pages, paid search, or partners who agree to keep it exclusive.

Contact rates are higher when there is no shared bidding. Costs are 2 to 4 times the shared pricing. Auto runs $30-$80. Health runs $50 to $120. Life runs $60 to $150. Final expense runs $40 to $90.

You need to verify exclusivity. “Exclusive” is a sales claim. Get it in writing. Audit it. Vendors sometimes sell the same lead twice, even after charging the premium.

Channel 3: Live Transfers

A screener reaches the buyer first. They check intent and basic eligibility. Then they pass the live call to the closer. The agent gets a warm call, not a form to dial.

Live transfers close at the highest rate among all lead types. Auto runs $35-$55. Health and life run $50 to $90. Final expense and Medicare supplement run $55 to $85. Live transfers wipe out the speed-to-lead variable. The buyer is already on the line.

Channel 4: Direct Mail Response

Mail campaigns target specific groups. Final expense aims at ages 65+. Medicare is available to those aged 65 and older. Life mail goes to homeowners and new parents. The buyer calls in or sends back a reply card.

Buyers who respond have raised their hand. That makes them higher intent than passive leads. Close rates run higher than mass channels. Volume is capped. Setup costs are higher. Final expense and Medicare supplement are the verticals where direct mail pays off.

Channel 5: Paid Search

Google and Bing ads catch buyers in active search. Terms like “car insurance quotes,” “affordable health insurance,” and “life insurance for seniors” pull ready people. They land on an owned page and submit info.

Intent is strong. CPCs are some of the highest in any field. Auto CPCs run $15 to $80. Health CPCs run $20 to $100. Cost per lead is often higher than aggregator pricing. But the intent makes up the gap for agencies that close at top rates.

Channel 6: Facebook and Social Lead Forms

Targeted lead forms collect info inside the app. The buyer never leaves the platform. Native forms convert better than off-platform pages.

Volume is moderate. CPL is moderate. Facebook works best for final expense and Medicare supplement. The platform is heavily used by the 55- to 75-year-old age group. Auto and health Facebook leads carry lower intent. The buyer was not searching when they saw the ad.

Channel 7: SEO and Organic Content

Teaching and comparing content ranks in search and pulls organic traffic. Forms and CTAs on the page turn that traffic into leads.

This channel has the lowest cost per lead. There is no per-lead fee, just content cost. The trade-off is time. It takes 12 to 24 months to see real volume for tough insurance keywords. SEO is a long bet. Run it next to faster channels, not in place of them.

Channel 8: Referral and Cross-Sell

Current policyholders and partners, like mortgage brokers, real estate agents, and auto dealers, send warm leads. So does cross-selling to current clients.

Referrals close at the highest rate of any source. They land at 30 to 60 percent versus 5 to 15 percent on internet leads. Cost per lead is near zero. The size of the client base caps Volume. Referrals have the highest ROI but the lowest scale. They support paid sources at the growth stage, not replace them.

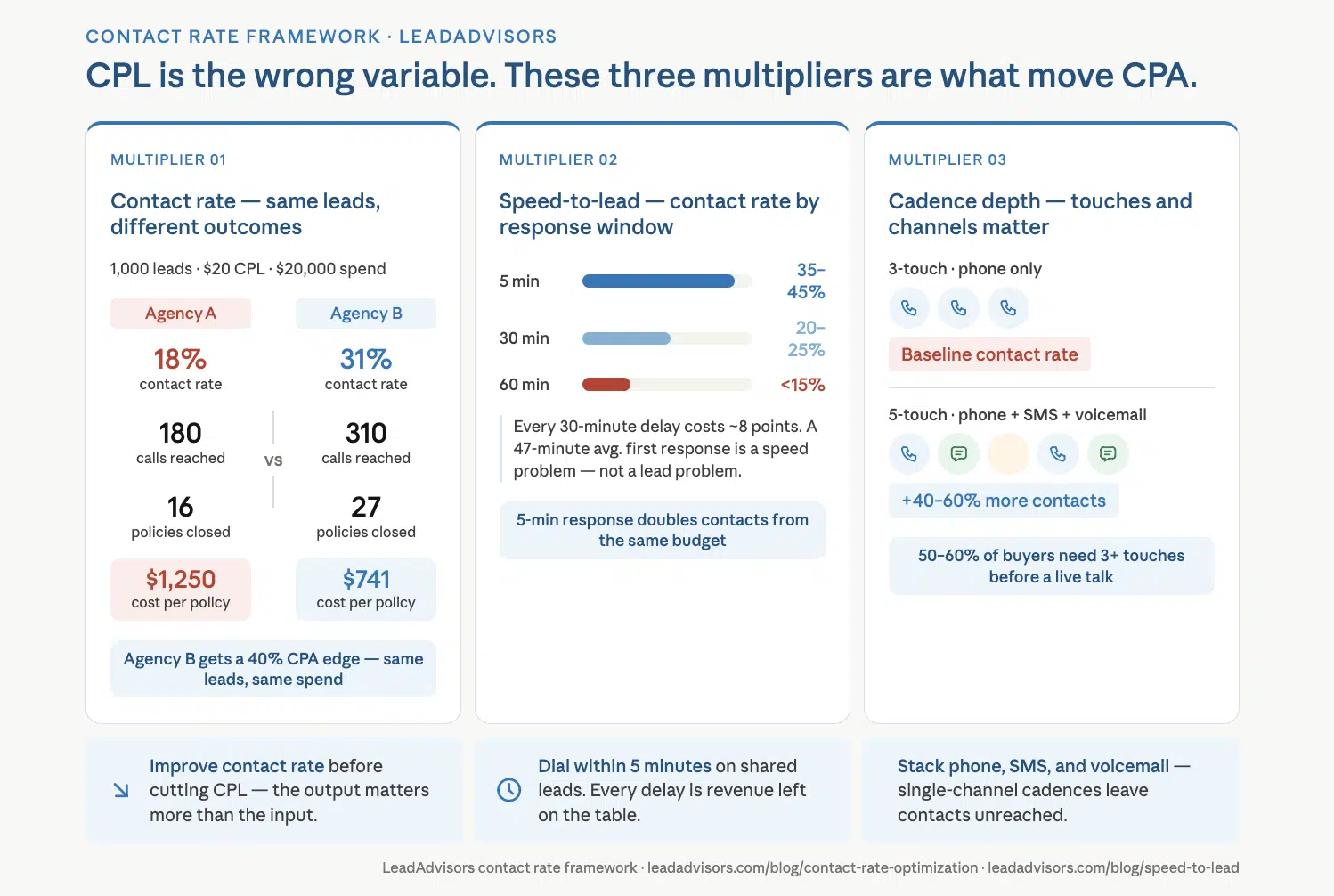

The Contact Rate Framework: Why Cost Per Lead Is the Wrong Variable

The most common mistake is chasing low CPL. CPL is just the input. Contact rate, qualified rate, and close rate are the outputs.

The Contact Rate Multiplier

Two agencies buy the same 1,000 leads at $20 each. That is a $20,000 spend.

Agency A reaches 18 percent (180 calls). Agency B reaches 31 percent (310 calls). Same leads. Same spend. Agency B gets 72% more calls with the same inputs.

At a 40 percent qualified rate and a 22 percent close rate, Agency A closes 16 policies. Agency B closes 27. Agency B’s cost per issued policy is $741. Agency A’s is $1,250. The contact rate gap alone gives a 40 percent CPA edge.

The Speed-to-Lead Multiplier

Response within five minutes drives contact rates of 35 to 45 percent on shared leads. At 30 minutes, they drop to 20-25 percent. After 60 minutes, they fall under 15 percent. Each 30-minute delay drops the rate by about eight points.

An agency with a 47-minute average first response does not have a lead problem. It has a speed problem. The same leads dialed in 5 minutes would double the number of calls from the same budget.

The Cadence Depth Multiplier

A single dial leaves most contactable leads on the table. Industry data shows 50 to 60 percent of buyers need three or more touches before a live talk. A five-touch plan covering phone, SMS, and voicemail beats a three-touch phone-only plan by 40 to 60 percent more contacts.

Improve speed, cadence depth, and channel mix. That moves more revenue than any drop in CPL.

Insurance Lead Costs by Vertical: The 2026 Benchmarks

| Lead type | Shared CPL | Exclusive CPL | Live transfer cost |

| Auto insurance | $8–$25 | $30–$80 | $35–$55 |

| Health insurance | $15–$40 | $50–$120 | $50–$90 |

| Life insurance | $20–$50 | $60–$150 | $55–$95 |

| Final expense | $10–$30 | $40–$90 | $55–$85 |

| Medicare supplement | $15–$45 | $55–$130 | $60–$100 |

| Home insurance | $12–$35 | $45–$100 | $40–$70 |

The same posted CPL can hide very different lead quality. A $15 health lead from a real carrier comparison site is not the same as a $15 health lead from content arbitrage on an unrelated article. The first hits 30 to 40 percent contact rates with strong intent. The second hits 10 to 15 percent contact rates with weak intent on the ones you reach.

Before you buy, do not ask “What is the CPL?” Ask “what source made this lead, what did the buyer do, and how many other buyers got the same lead at the same time.”

Building vs. Buying Insurance Leads: When Each Model Makes Sense

The build-vs-buy decision is not all-or-none. Most growth-stage agencies run both. They shift the mix as their own channels mature.

Buy leads when the agency needs volume fast. A new agent class, a new market, or an AEP push all call for buying. Bought leads bring pipeline now. They skip the 12-to-18-month wait that owned channels need. They also give a market signal. You learn which verticals, sources, and groups pay off before you invest in owned lead gen.

Build owned lead gen when the agency has 12+ months of bought-lead data on what works. The agency can wait 12 to 18 months for content and paid search to pay off. The agency operates in high-CPC fields like auto paid search or Medicare supplement, where CPCs exceed $50. In those markets, owned leads beat paid vendors every time.

The hybrid model most agencies run. Bought leads pay for today. Owned leads get built next to them. The shift happens over 18 to 36 months. Agencies at $5M+ in premium often run 40 to 60 percent owned and 40 to 60 percent bought. The owned base pulls down blended CPL. The bought base keeps volume flexible.

The 2026 TCPA and Compliance Reality

The Eleventh Circuit vacated the FCC’s one-to-one consent rule in Insurance Marketing Coalition Limited v. FCC, 127 F.4th 303 (11th Cir. 2025). The FCC then removed it from the rules in July 2025, as noted in its removal notice. Lead aggregators no longer need seller-by-seller consent at the federal level.

What did not change: the underlying TCPA framework, FCC robocall enforcement, FTC Telemarketing Sales Rule rules, state AG action, and private class action exposure.

What got tighter in 2025:

- The FTC’s August 2025 settlement with Assurance IQ and MediaAlpha totaled $145 million. It is the largest health insurance lead gen action in recent memory. Both firms were charged with misleading buyers about coverage and with using telemarketing and robocalls.

- The FCC removed more than 1,200 non-compliant voice service providers from the Robocall Mitigation Database in August 2025.

- Insurance and healthcare ranked second in 2025 robocall complaints to the FCC, accounting for 11 percent of total volume, per the FCC’s 2025 top-five robocall scam report.

- The FTC’s 2026 biennial Do Not Call Registry report confirmed 173 lawsuits against 570 companies and 449 people. Nearly $400 million has been collected since the registry began.

For Medicare-adjacent work, CMS finalized CY 2026 Medicare Advantage and Part D policy and technical changes in April 2025 (CMS-4208-F). The rule updated agent and broker pay and marketing rules. Medicare lead gen runs under a separate, stricter regime on top of TCPA.

What this means for agencies buying leads in 2026:

- Consent docs still need to be auditable by source. The federal one-to-one rule is gone. State laws, plaintiffs’ bar reads, and FTC disclosure rules are not.

- Every aggregator deal needs source-level transparency on consent and origination.

- DNC scrubbing and STIR/SHAKEN are baseline. Not a feature.

- The class action curve in insurance has not flattened. It has shifted from one-to-one cases to broader claims of misleading conduct and weak consent records.

The bar in 2026 is higher than it was before the rule was vacated. Enforcement shifted from a single rule to a broader pattern of rigor in disclosure and consent.

“Buying Insurance Leads”: Why the Search Term Is Common and Why the Pure Lead-Buying Model Is Broken

Searches like “buy insurance leads,” “cheap insurance leads,” and “insurance leads for sale” reflect how the field has been sold for two decades. Vendors built their model on agents paying per lead, dialing them, and closing some. It works on a small scale. It breaks at a large scale.

The real problems with the pure buy model:

- Same-lead bidding. A shared lead reaches three to eight buyers simultaneously. Dial speed picks the winner, not lead quality.

- No control over source. You do not pick the traffic source, the disclosure language, or the other offers the buyer saw before they submitted.

- Per-lead pricing puts the risk on you. The vendor gets paid regardless of your contact rate or close rate. You absorb all the risk.

- Volume cliff at scale. Push two to three times your normal volume from one vendor, and lead quality drops. The vendor fills the gap with lower-tier sources.

Agencies that earn a margin in 2026 are not the ones finding cheap leads. They are the ones building their own funnels (owned landing pages, paid search, exclusive partners, content). The bought supply becomes a lever, not a lifeline. Agencies still buying every lead are racing the dial. Agencies dialing their own exclusive leads are winning that race.

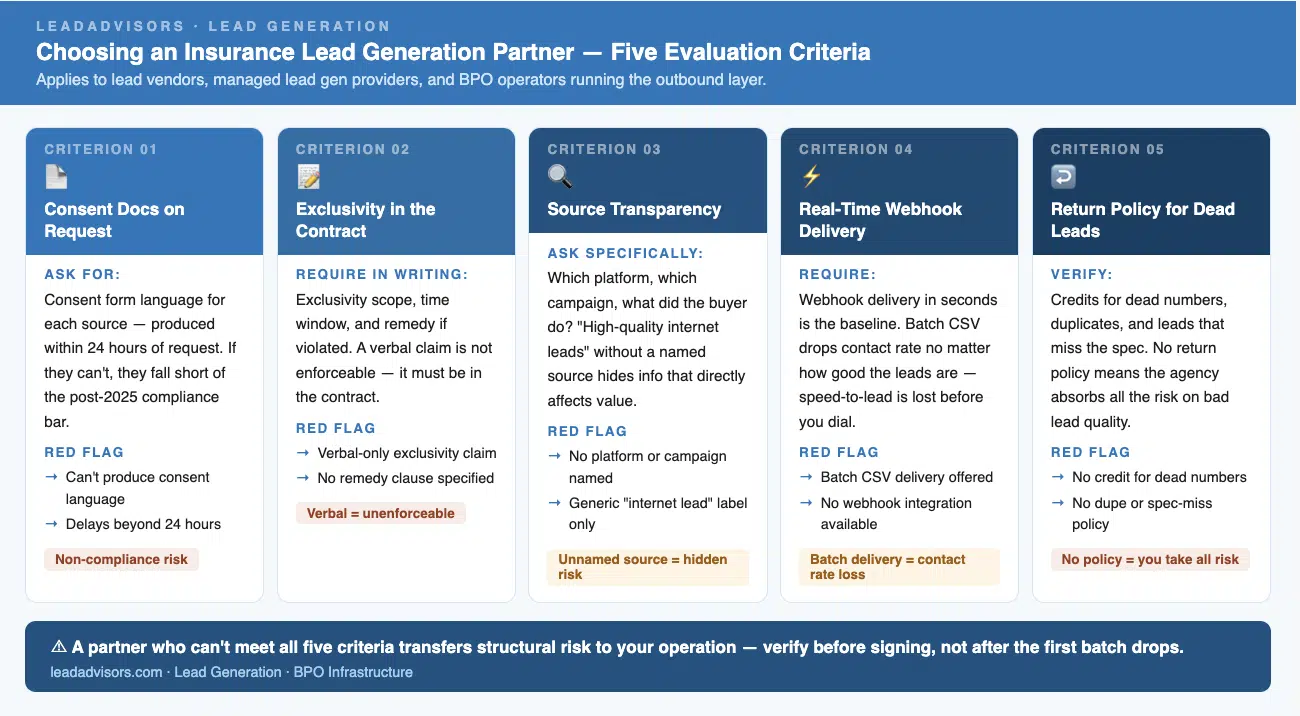

Choosing an Insurance Lead Generation Partner: Five Evaluation Criteria

The partner may be a lead vendor, a managed lead generation provider, or a BPO operator running the outbound layer. These five criteria reduce most structural risk.

- Consent docs on request. Any lead vendor must produce the consent form language for each source within 24 hours of request. If they cannot, they fall short of the post-2025 bar.

- Exclusivity in the contract. Exclusivity claims must be in writing. Spell out scope, time window, and remedy if violated. A verbal claim is not enforceable.

- Source transparency. Where do these leads come from? Which platform? Which campaign? What did the buyer do? A vendor who calls leads “high-quality internet leads” without naming the source is hiding info that affects value.

- Real-time webhook delivery. Leads that arrive late lose the speed edge before you can dial. Webhook delivery in seconds is the baseline. Batch CSV drops contact rate, no matter how good the leads are.

- Return policy for dead leads. A real vendor credits you for dead numbers, dupes, and leads that miss the spec. No return policy means you take all the risk.