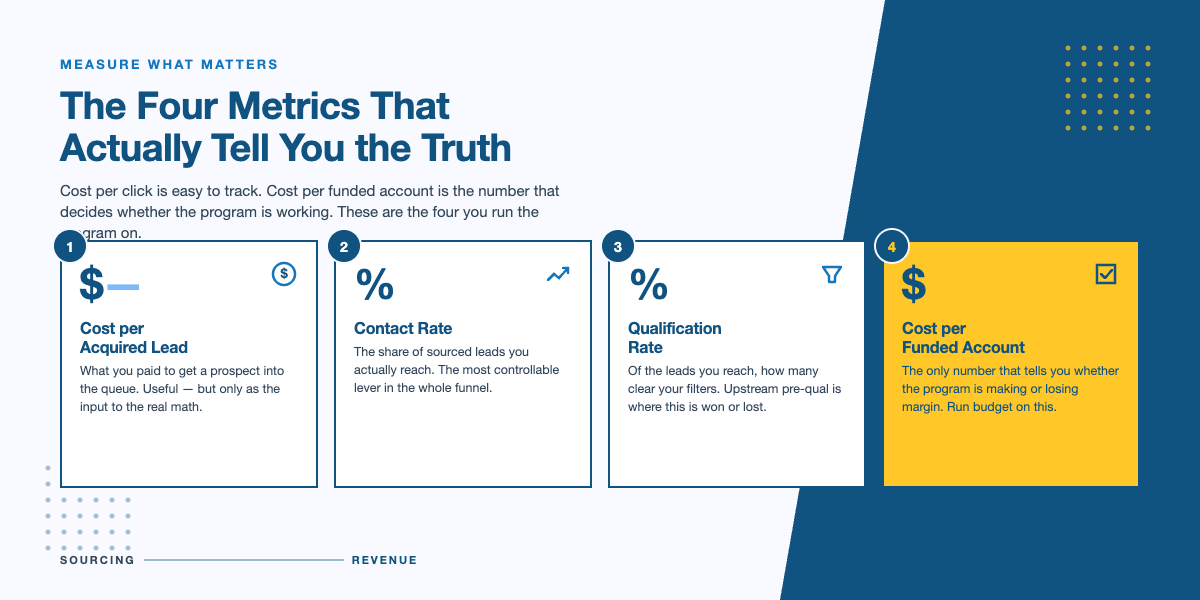

Most financial services lead programs are built around the wrong metric. Cost per click and cost per lead are easy to track. Cost per funded account is the number that actually tells you whether the program is working. The gap between those two metrics is where most operators lose margin without knowing it.

TCPA settlements, carrier spam flags, and state calling rules have made cold outreach in financial services harder every year for the past decade.

The operators who still hit their numbers in 2026 are not working harder. They are measuring different things.

What Financial Services Lead Generation Looks Like at Scale

A solo financial advisor uses lead generation to fill a meeting calendar. An operator running a debt settlement, personal loan, or mortgage business has a different problem. The scale is larger. The stakes are higher. The metrics that matter are not the same.

You source leads across multiple channels simultaneously. You measure each channel by funded account rate, not just lead count. You manage a contact team or decide whether to outsource that function based on the contact rate each channel produces.

And you do all of this under compliance rules that govern how, when, and how often you can reach a prospect.

The four metrics that matter most are cost per acquired lead, contact rate, qualification rate, and cost per funded account. A lead that costs $40 to acquire but converts at 2% is more expensive than a lead that costs $90 and converts at 8%. Operators who track acquisition cost but not funded account rate often do not see where their margins are going.

The Buyer Journey for Financial Services Leads

Before you build a strong lead program, you need to know how your prospects move from problem to purchase. Their path is not straight. Most of them look at several options before they talk to anyone. Knowing where they are in that process helps you reach them at the right time with the right message.

How Prospects Enter the Funnel

Most financial services leads enter the funnel through search. A person searching “how to settle credit card debt” or “personal loan for bad credit” knows they have a problem. They are looking for a solution. That is your entry point.

The challenge is that the same search query shows your landing page, a competitor’s page, an affiliate site, and a comparison tool. The prospect may fill out two or three forms before deciding whom to talk to. Speed to contact is not a competitive edge at that point. It is the minimum.

The Role of Trust Before Conversion

Money decisions are high-trust decisions. A prospect dealing with debt stress or a lending choice is asking one question before they answer a second call: Is this company real? Brand presence, reviews, and content all factor into that answer.

This is why organic search presence matters even for operators who mostly buy leads. Your brand’s online footprint affects the conversion rate of every lead you source, no matter the channel.

B2B Financial Services Buyers Need More Touchpoints

If you sell to business buyers, such as CFOs evaluating loan products or HR directors reviewing employee financial programs, the sales cycle is longer. These buyers research across many sources before they contact a vendor. White papers, case studies, and compliance records are not optional. They are part of what earns the call.

15 Financial Services Lead Generation Strategies

There is no single tactic that builds a strong lead program. It takes a set of systems working together. Each strategy below handles a specific part of the funnel. Some focus on where leads come from. Others focus on how you reach them. A few focus on what happens when your contact rate stalls.

Start with the strategies that match your biggest gap right now. Add more as each layer starts to work.

1. Define Your Qualification Profile Before Sourcing

The most common source of wasted lead spend is buying leads before you know what a qualified lead looks like. In financial services, that profile is specific. It includes credit score ranges, debt amounts, loan-to-value ratios, employment status, and state rules. If those filters are not set at the campaign level, every channel will send a mixed group. Your contact team will spend time on leads that should never have entered the queue.

Build the profile first. Apply it to form fields, pre-qualification questions, and channel targeting before you spend a dollar.

2. Invest in Organic Search for Inbound Lead Quality

Paid lead costs in financial services are high. High-intent keywords in debt settlement, mortgage, and personal loans can cost $30 to $80 per click in competitive markets. Inbound leads from organic search tend to convert at higher rates than purchased leads. The prospect found you based on your content. They were not just matched to the first form on a comparison site.

Organic search is a long-term investment. It does not replace paid sourcing in the short term. But it lowers your blended cost per acquisition over time. It also produces leads who already know your brand before the first call.

Content strategy for operators should focus on high-intent search terms tied to your product, compliant educational content that builds trust, and landing pages built to capture leads at the bottom of the funnel.

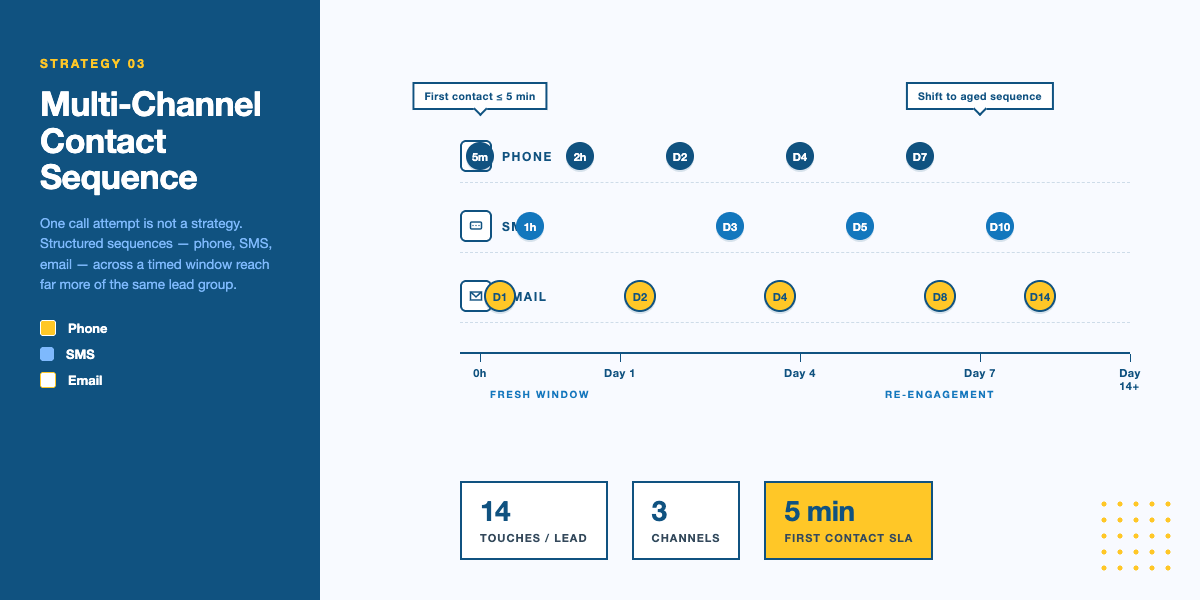

3. Build a Multi-Channel Contact Sequence

One call attempt on a new lead is not a contact strategy. Contact rates on single-touch outreach in financial services are low. Operators who run structured sequences, combining phone, SMS, and email across a set window, reach far more of the same lead group.

The design of the sequence matters as much as the channels you use. First contact should happen within minutes of a form submission. Follow-up attempts should be spread across different times of day and days of the week. SMS and email keep your brand in front of the prospect between call attempts. When they do answer, the call is not cold.

Compliance governs every part of this sequence. TCPA rules, state calling limits, and consent records must be built into the sequence before it runs.

4. Optimize Contact Rate as a Primary Metric

Contact rate is the share of sourced leads you actually reach. It is one of the most controllable numbers in your funnel. It is also one of the least tracked. Operators who measure cost per lead but not contact rate cannot find where their funnel is breaking down.

Contact rate is shaped by lead source quality, speed to first contact, call timing, caller ID health, and how well you follow contact frequency rules. Each of those is measurable. Each can be improved. A 10-point gain in contact rate on a high-volume program cuts cost per funded account without changing your sourcing budget.

5. Evaluate Live Transfer as a Sourcing Channel

A live transfer delivers a pre-screened, consented prospect directly to a closer the moment they pass qualification. The prospect is on the phone. They have already cleared your initial filters. Your closer gets a warm handoff instead of a cold call.

Live transfers cost more per lead than a raw form submission. That cost is often offset by a higher close rate and the removal of contact spend on leads that would have aged out. For operators with strong closing teams but limited contact capacity, live transfers can be a better use of the sourcing budget than high-volume raw-lead buys.

When evaluating a live transfer program, focus on the qualification layer. If the pre-qualification standards are too loose, the higher cost per transfer will not be covered by the conversion rate.

6. Use Pay-Per-Call Affiliate Networks for Intent-Verified Traffic

Pay-per-call programs bill per connected call, not per lead or click. The prospect placed the call. Intent is shown before the cost is charged. For debt settlement, mortgage, and personal loan products, pay-per-call networks can deliver high-intent traffic with contact already confirmed at the point of billing.

Compliance rules for pay-per-call in financial services are strict. Affiliate publishers must use compliant ad copy and proper consent language. Call recordings should be reviewed regularly. State limits on certain financial products require geo-filtering at the campaign level.

7. Segment Lead Campaigns by Product and Qualification Tier

Running a single broad campaign across a wide group produces a lead mix that is hard to work with. Segmenting by product type, qualification tier, and state rules lets your contact team focus outreach, use the right script, and route leads to the right closer.

For operators running debt settlement alongside a related product, such as personal loans or credit monitoring, cross-sell segments provide a second path for leads who do not qualify for the main product. A lead below the debt threshold for settlement may still qualify for a loan. Without segments, that second path does not exist.

8. Run Pre-Qualification at the Landing Page Level

Form-level pre-qualification filters out ineligible leads before they reach the contact queue. A prospect who does not meet your minimum debt threshold, or who is in a state where your product is not available, costs money to contact and earns nothing.

Pre-qualification questions on a form reduce lead volume but raise the qualification rate. The tradeoff almost always works in your favor at scale. Operators who resist pre-qualification to protect their conversion rate are measuring the wrong thing. Form fills are not the goal. Funded accounts are.

9. Manage Aged Lead Groups Separately

Leads past the initial contact window do not respond to the same sequence you use on fresh leads. Running day-one outreach on a 30-day-old lead produces low contact rates and wears out your list faster.

Aged leads need a re-engagement approach. New content, a different channel, or an updated offer. Some operators run re-engagement campaigns for aged groups via email or SMS with a fresh entry point, such as a rate update or a new qualifying question, before trying a phone contact.

10. Build Content Authority for Brand-Level Trust

Operators who buy most of their leads still benefit from content. A prospect who gets an outbound call from a brand they have seen in search, on review sites, or in an article answers at a higher rate. They convert at a higher rate, too.

Content for operators should be practical and direct. Write about the financial problems your product solves. Be clear about your process. Show your credentials and compliance standing. This is not a replacement for paid sourcing. It raises the conversion rate on everything else in your funnel.

11. Use Retargeting Across the Sourcing Funnel

Prospects who visit a landing page and leave without filling out a form have shown intent. Retargeting campaigns follow those visitors across display and social placements. For high-cost financial products where a decision can take days, retargeting recovers a share of traffic that would otherwise leave for good.

Retargeting in financial services requires a compliance review of ad copy. Some platforms also limit targeting options for certain financial product types.

12. Use Lead Scoring to Set Contact Queue Order

Not all leads in your queue have the same chance of converting. A lead who filled out a full pre-qualification form, came through organic search, and was submitted during business hours has a different priority than one who partly filled out a form at midnight via a broad display ad.

Lead scoring assigns weighted values to signals, then sorts the queue. Closers make first contact on the highest-value leads while those leads are still in their decision window. Lower-scored leads receive follow-up with lower priority. This does not reduce the total number of contact attempts. It sequences them so the best outreach happens first.

13. Connect CRM and Contact Systems for Full Funnel Visibility

Operators managing leads from multiple channels need a CRM that links sourcing data to contact results to conversion events. Without that link, you cannot calculate the funded account rate by channel, find which sources produce the best leads, or flag channels that bring volume but no revenue.

The CRM should capture lead source, submission time, qualification data, contact-attempt log, outcome for each attempt, and conversion result. That data set is what lets you manage the sourcing budget based on performance, not assumptions.

14. Monitor and Protect Caller ID Reputation

Caller ID health directly affects contact rate. Numbers flagged as spam by carrier platforms get rejected before the prospect sees who is calling. In high-volume outreach, numbers can get flagged fast. That damage is not always visible without active monitoring.

Maintaining contact rate means rotating numbers before they hit flagging limits, watching reputation scores across carriers, and keeping calling behavior within the rules that trigger spam labels. This is a core operational task for any financial services contact team running outreach at volume.

15. Build BPO Contact Operations Around Financial Services Compliance

Outsourcing your contact and qualification work to a BPO without financial services experience creates compliance risks and hurts conversion rates. Financial services scripts, disclosure rules, and state limits require a team that knows the regulatory context, not just the dialing mechanics.

If you outsource the contact function, your BPO should have documented compliance training, call recording and QA processes, and a clear path for raising contacts that create regulatory flags. The cost of a compliance failure in financial services outreach is higher than the cost of choosing a better contact partner from the start.

Lead Generation for Fintech Lenders and Credit Products

Fintech companies in lending and credit, including personal loan platforms, buy-now-pay-later products, and digital mortgage lenders, face the same sourcing and qualification pressures as other operators. But they carry an added burden. They have to prove that a new digital platform is as safe as a bank the prospect has used for years.

The 15 strategies above apply directly to fintech lenders. The points below are specific to the digital product context.

Earn Trust Before the Conversion Event

A prospect being asked to link a bank account or share income data through a new app has a higher security bar to clear than one walking into a branch. Security marks, clear data-handling disclosures, and transparent fee structures must be visible at every stage of the funnel, not just in the fine print.

Treat the App Store as a Search Channel

For consumer-facing lending or credit products in a mobile app, App Store Optimization works like organic search. Ranking for category keywords in the App Store brings in intent-verified traffic at a lower cost than paid acquisition on the same keywords through other channels.

Use Product-Led Acquisition Where the Product Allows

For credit monitoring or financial health tools that sit alongside a core lending product, a free entry point can build a qualified lead group at low acquisition cost. The path from free user to loan applicant needs a clear trigger and offer. It will not happen on its own.

Make Compliance Review a Step in Every Publishing Process

Financial services advertising is regulated at the federal and state levels. Claims about rates, approval odds, and terms carry disclosure rules. Fintech marketing that skips a compliance review before going live creates regulatory exposure. In a trust-dependent category, that exposure is hard to recover from.

Integrating Lead Generation with the Sales Funnel

Lead generation and the sales funnel are not two separate systems. They are one pipeline. A gap at any stage affects all subsequent stages. This section maps what each funnel stage needs from a lead generation program and what breaks when those needs are not met.

Top of Funnel: Sourcing and Qualification

The top of the funnel is where leads enter. The quality of what enters here shapes every stage below. Evaluate sourcing channels by qualified lead rate, not raw volume. Apply qualification filters as far upstream as you can. This reduces contact cost on leads that should never have been in the queue.

Middle of Funnel: Contact and Warm-Up

The middle of the funnel is where you reach the prospect and build enough trust for a real conversation. Multi-channel sequences, lead scoring, and contact rate all happen here. The goal is to reach the prospect while their intent is still active. Every day without contact is a day a competitor could get there first.

Bottom of Funnel: Conversion and Funded Account

The bottom of the funnel is the conversion event: a completed application, an approved loan, or a signed agreement. Cost per funded account is the metric that matters here. Operators who track conversion events back to the sourcing channel have the data to move budget toward what is producing revenue.

Automation and Lead Nurturing

Automation handles follow-up with leads that have been contacted but have not yet converted. Email sequences, SMS reminders, and retargeting ads keep your brand top of mind during the decision period. Set automation to respond to behavior, such as a return visit to the pricing page or an opened email, rather than a fixed schedule that runs regardless of the prospect’s actions.

Common Mistakes in Financial Services Lead Generation at Scale

Even well-run programs break down in predictable ways. These are the mistakes that show up most often and cost the most to fix.

Optimizing for lead volume over qualification rate. High volume at a low qualification rate raises the cost per funded account. It also adds work to your contact team without matching revenue growth.

Not tracking contact rate. Contact rate is one of the most controllable numbers in the funnel. Operators who do not track it cannot find where performance is breaking down between sourcing and conversion.

Making one call attempt and stopping. One call is not a strategy. Multi-channel, multi-attempt sequences are needed to reach strong contact rates in financial services.

Sourcing leads without checking consent records. Consent failures in financial services outreach create TCPA exposure. Verify that consent was collected at the source and that it covers the contact methods you plan to use.

Running the same sequence on fresh and aged leads. A 45-day-old lead does not respond the same way a same-day lead does. Aged groups need a separate re-engagement approach.

Ignoring brand presence. Brand authority affects both contact and conversion rates for paid leads. Operators who source only through third-party channels without any brand investment pay full price for leads that convert below their potential.

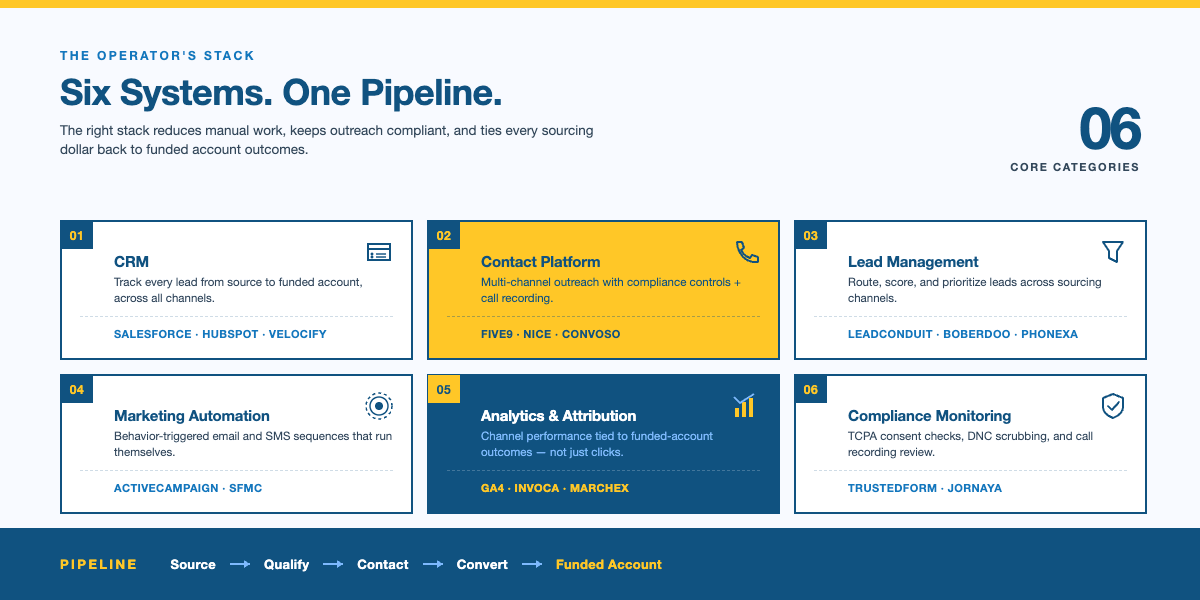

Tools and Technology Stack

The right tools reduce manual work, improve data visibility, and ensure your contact operations remain compliant. The table below covers the core categories and common options for each.

What to Expect in 2026

AI-assisted lead scoring will become standard. Large operators already use models that score leads based on behavior and data signals. As these tools become more available, operators without lead scoring will fall behind on contact efficiency.

First-party data will matter more. Rules around third-party data have been tightening for years. Operators who have built first-party data assets through inbound content, organic search, and owned lists will have a more stable sourcing base than those who rely only on purchased data.

Contact rate pressure will grow. Carrier spam detection, TCPA litigation, and rising awareness of unwanted calls are all driving down contact rates. Operators with compliant, multi-channel contact systems will hold their numbers. Those running high-volume single-channel outreach will see a steady decline.

Compliance requirements will expand. State-level financial services rules keep moving into areas that once ran under federal-only standards. Operators who treat compliance as an ongoing operational task will absorb those changes without disrupting their contact programs.

How LeadAdvisors Builds and Runs Lead Generation Systems for Financial Services Operators

LeadAdvisors works with debt settlement companies, personal loan lenders, and mortgage operators that are deciding whether to build or outsource their contact and qualification systems. The work is operational. We build the system and run it.

BPO Contact Strategy. We design and operate multi-channel contact sequences for financial services lead groups. That includes contact-attempt structure, compliant script development, caller-ID health management, and QA built for a regulated outreach environment. We are accountable to a contact rate metric, not to a set of steps for your team to follow.

Live Transfer Programs. For operators who want pre-qualified, consented prospects sent directly to a closer, we run live transfer programs built around your qualification criteria. The upstream qualification layer verifies that your minimum standards are met before a transfer is billed.

Lead Qualification and Scoring. We build qualification frameworks that apply your filters during sourcing. This reduces the number of bad leads entering the contact queue. For operators with mixed lead groups, we set up scoring models that sort the queue by conversion probability.

Inbound Lead Generation through Organic Search. We build and manage content and SEO programs for operators who want an inbound channel alongside paid and affiliate sourcing. The content strategy is built around the search terms your qualified prospects actually use.

Analytics and Funded Account Attribution. We connect sourcing data to conversion outcomes so you can see cost per funded account by channel, not just cost per lead. That data is what lets you move the budget toward what is producing revenue.