Your closers are on the phone most of the day. Half that time is spent chasing leads who submitted a form three days ago, don’t remember doing it, and have already talked to four other lenders. That is not a sales process problem. It is a lead quality problem.

Mortgage live transfers are designed to fix the front end. Instead of handing a team a cold list and hoping for the best, a live transfer places a pre-screened, currently engaged prospect on the phone and ready to talk. This guide covers how the process works, what is screened before a call reaches the floor, and what to look for when evaluating providers.

What Is a Mortgage Live Transfer?

A mortgage live transfer is a pre-qualified prospect who has been contacted by an outbound calling agent, following the same high-intent principles found in the ultimate guide to live transfer leads, and is warm-handed off in real time to a waiting closer.

This lead type is distinct from the three alternatives most commonly used on high-volume floors:

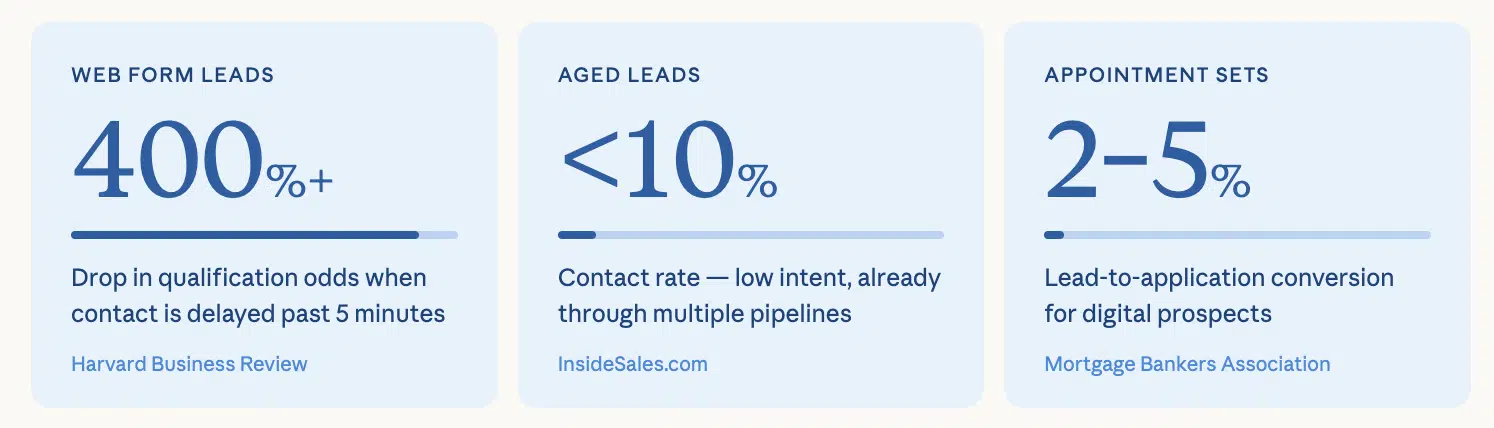

- Web form leads: By the time a closer dials back, between 5 and 60 or more minutes may have passed since the form was submitted. Research published by Harvard Business Review documents that the odds of qualifying a lead drop by over 400 percent when contact is delayed beyond five minutes of submission.

- Aged leads: These are re-contacted leads that have already passed through multiple lenders’ pipelines. Intent is low, and contact rates are documented at well below 10 percent in most campaigns.

- Appointment sets: While a future callback is scheduled, the industry faces significant hurdles in engagement; the Mortgage Bankers Association (MBA) reports that lead-to-application conversion rates typically hover between 2% and 5% for digital prospects, reflecting the high rate of attrition in the early stages of the mortgage process.

The structural advantage of mortgage live transfers is that the gap between prospect intent and closer conversation is collapsed to near zero, representing a major shift toward more effective lead management compared to traditional web forms. The prospect has been reached, screened, and is on the line. No window exists for intent to fade or for a competing lender to step in.

Why the 100% Contact Rate Is Structural and Not a Marketing Promise.

In every other lead type, a closer must initiate outbound contact. A contact rate exists because some dials succeed and others do not. Wrong numbers, voicemail, disconnected lines, and call screening reduce that rate to somewhere between 8 and 35 percent, depending on lead age and source quality.

In a live transfer, the outbound agent has already achieved contact. The prospect is on the phone. The closer does not dial anyone. They are connected to an already-active call.

The concept of a contact rate, as traditionally defined, does not apply because no outbound dial is made by the closer. The connection already exists. That is what makes the 100% contact rate a structural reality, not a performance claim.

How the Mortgage Live Transfer Process Works: Step by Step

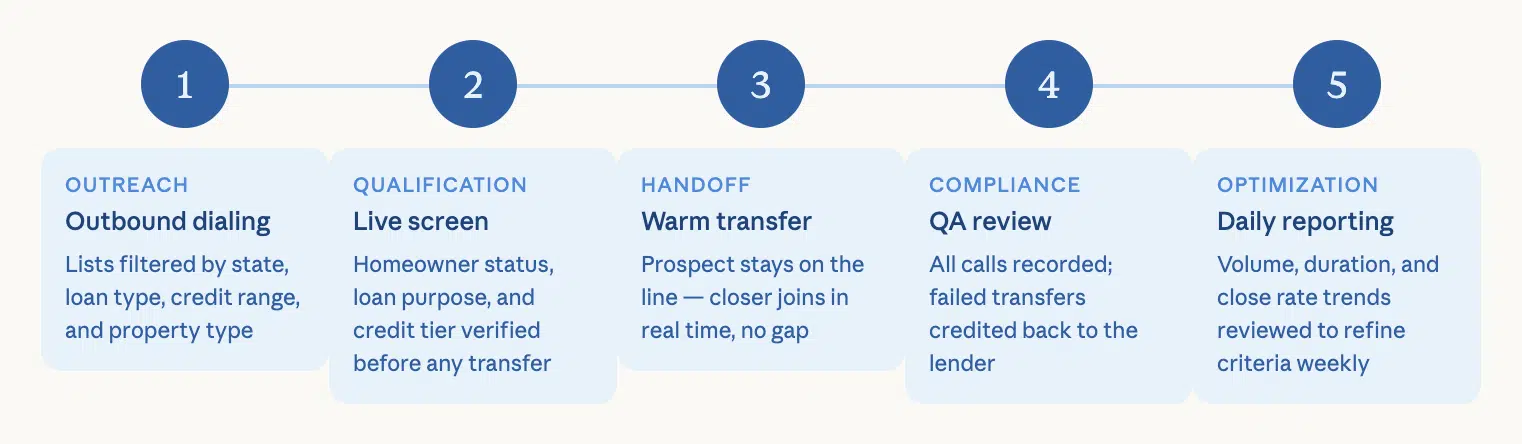

The following operational sequence describes how a properly managed live transfer program is run. Each step is designed to ensure that what reaches the closer is a qualified, compliant, and currently engaged prospect.

Step 1: Outbound Dialing Against Your Criteria

Lists are worked by trained outbound agents, filtered to target states, loan type, credit range, and property type. Daily volume is controlled by the lender’s transfer caps, so the floor is never overwhelmed or left waiting.

Step 2: Live Qualification Screen

Before any transfer is initiated, a scripted screen is run to ensure the prospect meets strict criteria, a process detailed in our breakdown of screening leads by qualification, covering homeowner status, loan purpose, and credit tier. If any criterion is not met, no transfer is made. This is the quality gate that protects closer time.

Step 3: Warm Handoff in Real Time

The prospect stays on the line while the closer is brought in. No callback is requested, no gap is introduced. The handoff happens while the prospect is engaged and expecting the conversation to continue.

Step 4: QA and Compliance Review

All calls are recorded and reviewable, adhering to rigorous call center QA and training standards to ensure that every transfer meets the agreed-upon quality benchmarks. Transfers that fail to meet the agreed criteria are credited back. This accountability layer ensures providers maintain consistent quality because they bear the financial cost of not doing so.

Step 5: Daily Reporting and Optimization

Transfer volume, average duration, disposition data, and close rate trends are reported daily. This feedback loop allows campaign criteria to be adjusted week over week rather than running on lagging indicators.

What Is Screened Before a Transfer Reaches Your Closer

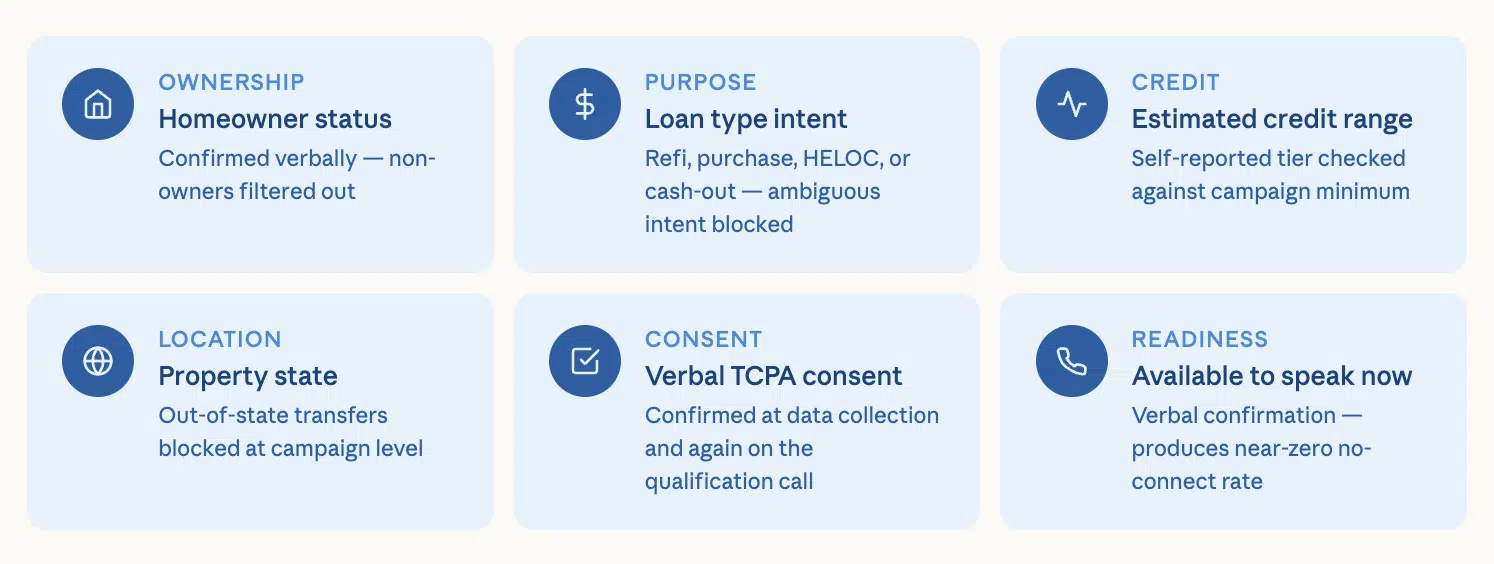

The most common quality objection about mortgage live transfers concerns what is actually verified before a call reaches the floor. A properly managed program screens the following six data points on every prospect before a transfer is initiated:

- Homeowner status: confirmed verbally. Non-owners are filtered out at this stage.

- Loan type intent: the prospect has stated their purpose, whether refinance, purchase, HELOC, or cash-out. Ambiguous intent does not result in a transfer.

- Estimated credit range: self-reported credit tier is captured and checked against the campaign minimum threshold.

- Property state: the transfer is made only if the prospect’s property falls within the lender’s licensed states. Out-of-state transfers are blocked at the campaign configuration level.

- Verbal TCPA consent: consent to be contacted is confirmed at the point of data collection and again during the qualification call.

- Availability to speak now: the prospect has verbally confirmed they are ready for a conversation. This is what produces the near-zero no-connect rate.

TCPA Compliance in 2025 and 2026

The FCC’s proposed one-to-one consent rule was vacated by the Eleventh Circuit Court of Appeals in early 2025, after the court found the agency exceeded its authority; the FCC subsequently issued a final order in August 2025 to formally strike the requirement and reinstate the prior standards for express written consent.

The reinstated standard requires that prior express written consent must be in writing, include the consumer’s signature, and contain clear disclosures. Lending floors must work with providers who can produce written consent records on request.

Separately, the FCC implemented stricter opt-out processing requirements effective April 11, 2025, requiring businesses to honor revocation requests within 10 business days across all channels. A managed transfer program that cannot demonstrate compliance with this standard represents a direct legal risk to the lender.

DNC list scrubbing must occur before any outbound campaign is initiated, not after. Both the federal National DNC Registry and applicable state-level DNC lists are required to be applied to.

LeadAdvisors maintains documented consent records on every transfer and can produce proof of consent on request. DNC scrubbing runs before any campaign is initiated, federal and state lists both. If a provider cannot confirm their scrubbing cadence and consent documentation in writing, they are a compliance liability, not a vendor.

Mortgage Live Transfers vs. Other Lead Types: The Real Cost Comparison

Per-transfer pricing is the most common reason lenders hesitate when evaluating this lead type. When cost is measured at the unit level, live transfers appear expensive compared to web form leads or aged data. When cost is calculated at the outcome level, meaning cost per closed loan, the math typically reverses.

The table below compares lead types across four operational dimensions:

Lead Type Comparison

Lead Type | Intent | Contact Rate | Closer Effort |

Live Transfer | High (Pre-screened) | 100% (Structural) | Minimal / Ready to Close |

Web Form | Medium | 15% – 30% | High (Chasing/Dialing) |

Aged Lead | Low | < 10% | Very High (Burnout Risk) |

Appt. Set | Medium-High | 55% – 70% | Moderate (No-shows) |

A closer chase of 60 aged leads might yield only five productive conversations in a day. In contrast, a closer receiving 15 live transfers gets 15 pre-qualified, engaged prospects. When you factor in labor, licensing, and overhead, the “cheap” aged leads actually cost more per connected conversation than premium live transfers.

With mortgage profitability hitting its highest point since 2021, lenders are under pressure to cut costs and boost output. High-volume floors that have shifted from manual re-contact dialing to managed transfer programs consistently report higher per-closer productivity and lower cost per closed loan. Replacing manual follow-ups with live transfers is the fastest way to increase closer productivity and protect your margins.

What Separates a Good Live Transfer Provider from a Bad One

Not all mortgage live transfer providers operate the same way. A meaningful distinction exists between marketplace models and high-touch managed call center outsourcing programs, where a dedicated team handles dialing, qualification, QA, and compliance. The following criteria are recommended for evaluating any provider:

Compliance Infrastructure

Federal and state DNC scrubbing is confirmed in writing. TCPA consent is documented at the data level, not assumed or verbal-only. As of April 2025, opt-out requests must be honored within 10 business days across all channels. A provider that cannot show this process in writing does not have it.

QA on Every Transfer

Calls are recorded and reviewable. A credit process exists for transfers that fail to meet the agreed criteria. If a provider will not credit bad transfers, they have no financial incentive to send good ones.

Transparent Reporting

Daily dashboards showing transfer volume, duration, and disposition are provided. When reporting is vague or delayed, transfer quality typically follows the same pattern.

Campaign Flexibility

Daily caps can be set, states can be filtered, and criteria can be adjusted mid-campaign. Rigid providers are typically running a pass-through model, not a managed one.

Operational Ownership

A team is in place managing the dialing floor, QA review, and the compliance layer. A software platform that routes a number with no human accountability is associated with measurably lower transfer quality.

Credit Policy in Writing

The provider has a documented policy for what constitutes a bad transfer and how credits are applied. Verbal assurances are not a substitute for a written SLA.

How to Set Your Closer Team Up for Live Transfer Success

Even high-quality mortgage live transfers will underperform if the receiving team is not operationally ready. Three areas account for most of the performance gap on the lender’s side.

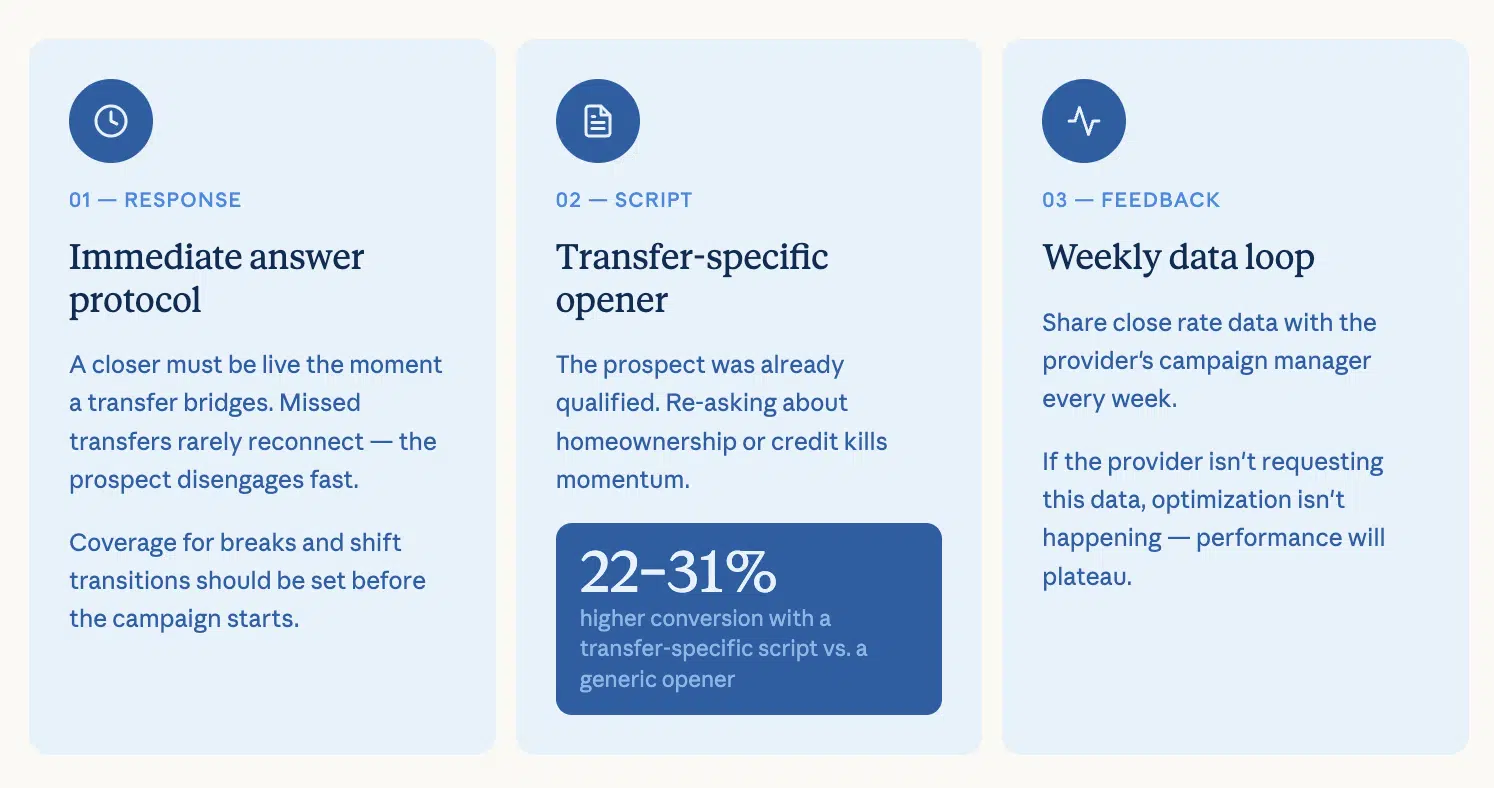

Immediate Response Protocol

A closer must be available the moment a transfer is bridged. Missed transfers rarely reconnect successfully. The prospect has already disengaged by the time a callback is attempted. Coverage protocols for breaks and shift transitions should be established before a live transfer campaign starts.

A Transfer-Specific Script

The prospect has already been qualified by an outbound agent. A closer who opens with basic discovery questions about homeownership status, loan purpose, and credit range is unknowingly re-running a qualification the prospect just completed. Momentum is lost. The opener should be written to pick up mid-conversation, acknowledge what was already covered, and move directly into value-added discussion.

Gong.io analysis consistently shows higher win rates among closers who open with context-specific language rather than generic discovery questions, and consistency in discovery-based patterns is the primary differentiator for high-performing closers in live transfer environments.

Feedback Loop with the Provider

Weekly close rate data should be shared with the provider’s campaign manager. A managed program should be using this data to refine qualification criteria and improve transfer-to-close ratios over time. If the provider is not requesting this data, optimization is not happening, and performance will plateau.

Key Takeaways

- Mortgage live transfers provide a guaranteed contact on every unit because the connection already exists at the moment of transfer.

- A six-point qualification screen is run before any transfer is initiated, covering homeowner status, loan purpose, credit tier, state eligibility, TCPA consent, and availability.

- When measured at cost per closed loan rather than cost per lead, live transfers consistently outperform web form and aged lead programs.

- The FCC’s revised TCPA consent standard, reinstated in September 2025, requires written prior express consent with clear disclosures. The April 2025 opt-out rule requires revocation to be honored within 10 business days across all channels.

- The MBA forecasts $2.2 trillion in single-family mortgage originations for 2026, up from $2.05 trillion in 2025. In a competitive origination environment, per-closer productivity is a direct profit lever.

- Closer-side readiness, including immediate response protocol, a transfer-specific script, and a weekly feedback loop with the provider, is equally important to outcomes as lead quality.

Ready to See Live Transfers on Your Floor?

LeadAdvisors runs managed mortgage live transfer campaigns through VLT. Transfers are pre-qualified, TCPA-compliant, and backed by QA review and daily reporting. The entry point is a 200-transfer test: no contract, no commitment beyond the pilot. Request pricing for your campaign criteria, and we’ll map the transfer volume to your floor capacity.